From Duopoly to Near-Monopoly: SportyBet Surpasses 50% Demand Share in Ghana

A regulated and fast-expanding iGaming market is rapidly turning into a one-brand story.

While the overall pie in Ghana keeps growing, the competitive order is shifting faster than many expected, with clear winners, visible losers, and surprising new entrants. Here’s what the latest Blask data reveals about regulation, football-driven seasonality, and the brutal battle for market share in one of West Africa’s most mature iGaming markets.

Blask metrics overview

- Blask Index — a real-time measure of market demand volume for iGaming brands in a given country, based on normalized search data.

- BAP (Brand’s Accumulated Power) — a brand’s percentage share of total market demand in a specific country and period.

Macro snapshot

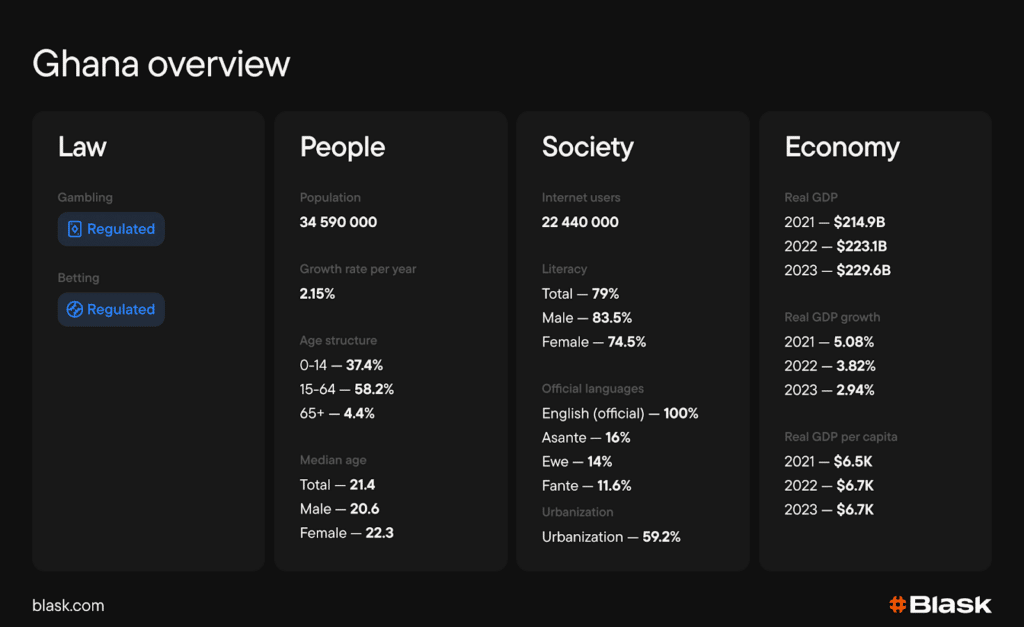

Ghana’s population stands at 34.59 million, with a median age of 21.4. Internet users number 22.44 million, representing a penetration rate of 64.9%. Mobile devices account for approximately 77% of all web traffic, making smartphone-based betting the primary access channel.

Regulation: a stable framework, tightening at the edges

Ghana’s iGaming market is open and fully regulated under a single national framework. The Gaming Commission of Ghana, established under the Gaming Act 2006 (Act 721), licenses and supervises all games of chance including sports betting, casinos, and online gaming. With approximately 90 licensed operators as of June 2025, the framework is functional, and stable enough to have allowed market concentration to accelerate without disruption.

Key timeline

- 2006 — Gaming Act (Act 721) establishes the Gaming Commission of Ghana as the sole regulator for all games of chance except lottery

- 2006 — National Lotto Act (Act 722) establishes the National Lottery Authority to regulate state lotteries separately

- August 2023 — Income Tax (Amendment) Act 2023 (Act 1094) introduces a 10% withholding tax on player winnings

- April 2025 — Income Tax (Amendment) Act 2025 (Act 1129) repeals the withholding tax on player winnings entirely

- June 2025 — A new 11-member Governing Board is inaugurated, with a mandate to modernise regulation and crack down on unlicensed operators

Tax stack

Operators pay a 20% GGR tax. The 10% withholding tax on player winnings, in place since August 2023, was abolished in April 2025, a move that reduces friction for bettors and supports activity in the regulated market.

Licensing runs through a single path

Foreign operators must register locally and maintain at least 10% Ghanaian shareholding. The Gaming Commission has signalled stricter enforcement against unlicensed operators and tighter zoning rules around schools and places of worship.

Read Also: Ghana’s casino shelf: Aviator steals the show

Market dynamics: steady climb, football-driven

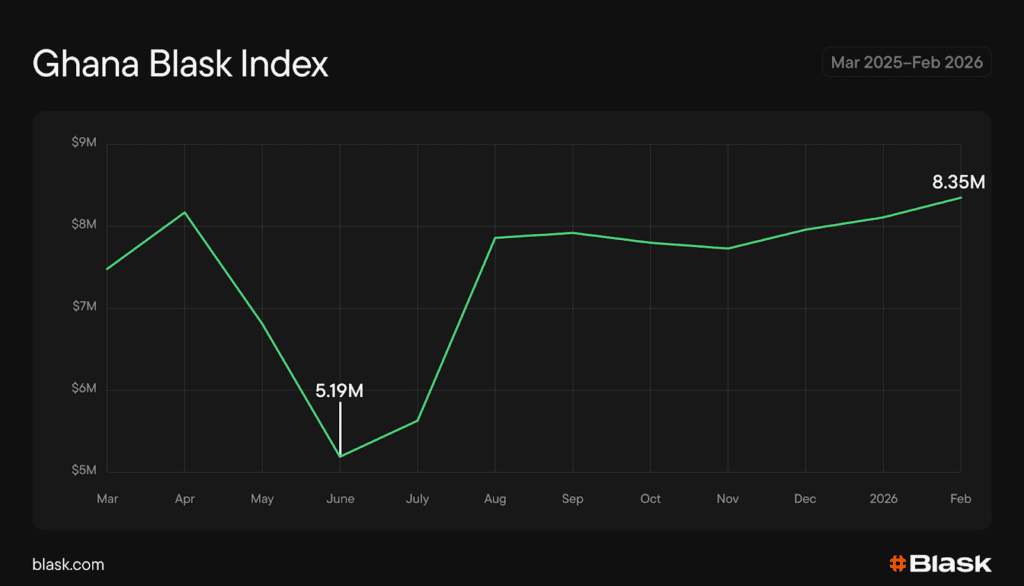

Ghana’s Blask Index moved in a pattern familiar across West Africa — shaped almost entirely by the European football calendar. The data period from March 2025 to February 2026 breaks into three distinct phases.

Mar–June: plateau then dip. Demand held relatively stable through the final stretch of the 2024–25 Premier League season, which concluded May 25, 2025. Once European leagues entered the summer off-season, activity eased — the weakest window of the entire data period falling in June and July as football-focused bettors pulled back.

Read Also: Kenya iGaming Market Overview: Growing Through the Reset

July–Sep: season launch surge. The return of club football drove a sharp recovery. The 2025–26 Premier League kicked off August 15, and the Champions League league phase opened September 16 — bringing simultaneous midweek and weekend fixtures that sustain betting volume at its highest cadence.

Oct–Feb: sustained elevation. Demand held at elevated levels through the second half of 2025 and into early 2026, buoyed by the full Champions League schedule running through January 28, 2026, and consistent Premier League matchweeks. No significant dip disrupted this stretch.

Competitive landscape: one brand breaks away, the challenger retreats

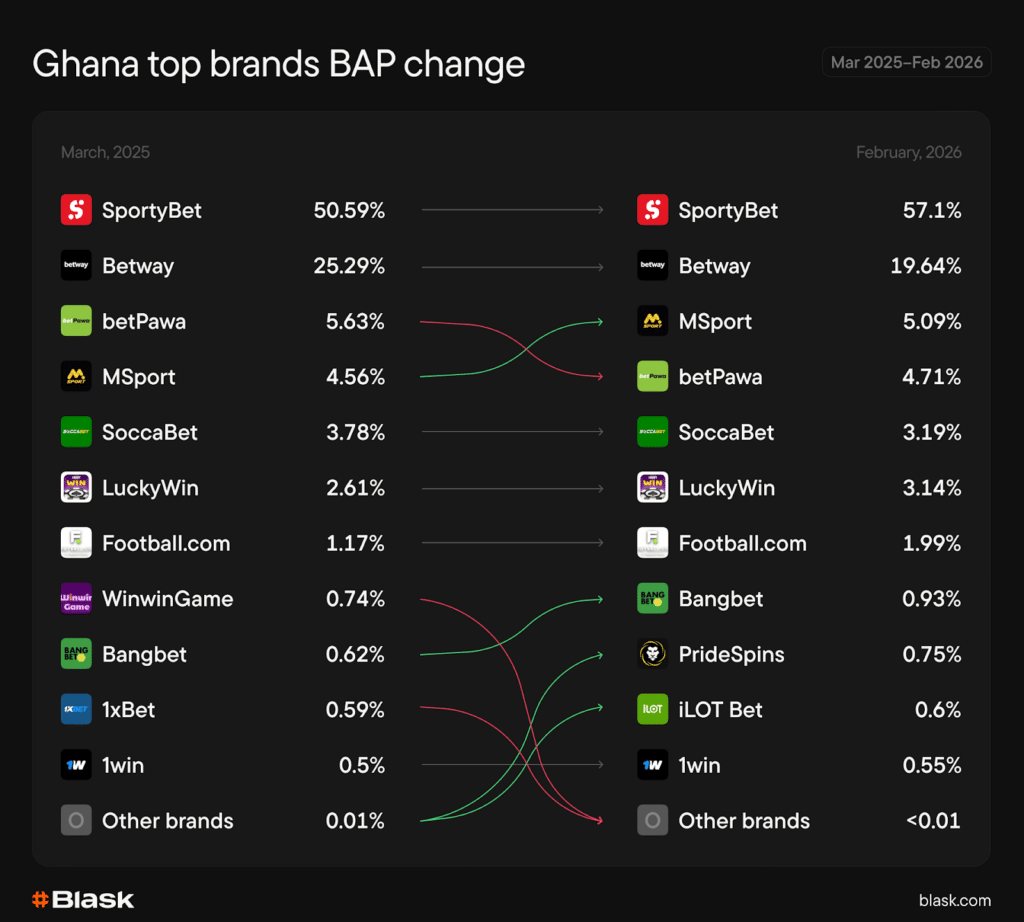

Ghana’s market is a duopoly in structure but increasingly a one-brand story. SportyBet and Betway together account for more than three-quarters of total market demand. SportyBet has extended its lead decisively while Betway has shed significant BAP, the most consequential shift of the data period. Below them, the rest of the field is fragmented and distant.

The top ten is not permanently fixed. Two brands dropped out of the ranking entirely over the data period while two new names, including PrideSpins, a locally licensed operator, broke in for the first time.

Locally licensed brands dominate. Nine of the ten brands in the February 2026 ranking hold Gaming Commission of Ghana licenses. The notable exception is 1win, which operates under a Curacao license. Other brands outside the top ten account for just 0.01% of BAP, for new entrants, the barrier is competitive, not regulatory.

Seasonality: Football Drives the Calendar

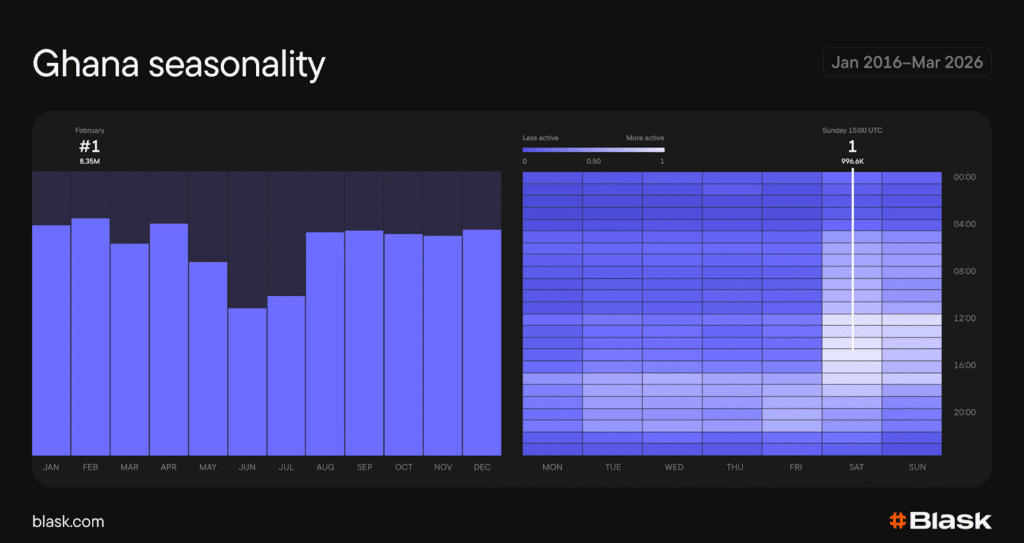

Ghana’s annual betting cycle follows the European football calendar closely. Activity builds from August as the Premier League kicks off, peaks through October to December when the Champions League group stage runs alongside a full Premier League schedule, then holds firm into January. The weakest window falls in June and July, when European leagues enter the off-season and demand visibly drops, the shortest bars of the entire annual cycle.

Weekend days are the clear peak, with Saturday and Sunday showing the highest activity across the heatmap, driven by Premier League matchdays and the accumulator betting culture they sustain. Weekdays are noticeably quieter, with activity building back toward the weekend.

Conclusion

Ghana’s iGaming market is regulated, concentrated, and consolidating fast. SportyBet commands 57.1% of BAP as of February 2026, a share that grew throughout the data period while the second-largest brand retreated.

Concentration does not mean the competitive order is sealed. Betway’s decline from 25.29% to 19.64% BAP shows that even globally recognised brands can lose ground when local operators outperform them. PrideSpins entered the top ten for the first time in February 2026, proving that new brands can break through, but only with the right product and the credibility of a local license.

Ghana rewards operators who commit fully to the market. The framework is open, the audience is growing, and the long tail is virtually nonexistent, meaning every percentage point of BAP ceded by an incumbent is a real and capturable opportunity.