Nigeria is fast becoming one of Africa’s most dynamic online-casino markets. Roughly 14,300 games are listed across about 180 active brands tracked by Blask. The catalog has grown in tandem with the country’s mobile-first gambling boom and a young, digitally native player base. Yet catalog breadth alone tells only half the story. The real competition plays out on the lobby’s front screen — the handful of tiles a player sees before scrolling.

Supply is dominated by a single provider’s slot franchise; demand, meanwhile, has been shaped by PG Soft’s Fortune series and Spribe’s Aviator — titles that barely register in the top-shelf distribution data. Understanding that tension is the key to reading the market correctly.

Blask metrics overview

- GVR (Game visibility rank) — daily ranking of game placement across operator lobbies. Blask scans lobbies daily, recognizes tens of thousands of games, and shows: how many brands carry each game, how often it appears in lobbies and other pages and at what average position.

- SoI (Share of interest) — search-based metric showing how much player interest each game captures in a market. Track shifts monthly — spot what’s trending up or cooling down.

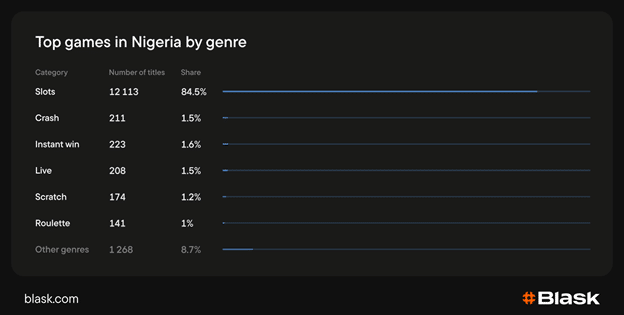

Genre distribution: a slots monoculture with pockets of variety

Slots account for 84.5% of the entire Nigerian catalog, making this an overwhelmingly reel-driven market. The remaining 15.5% is fragmented across several niche categories: Instant Win leads the secondary pack, followed by Crash, Live Dealer, Scratch, and Roulette. A catch-all “Other” bucket absorbs another 8.7%, covering everything from virtual sports and keno to specialty mini-games.

The genre mix reflects a familiar operator playbook: filling the catalog with slots to project depth, then sprinkling in crash and live-dealer options as session-type alternatives. What the genre split doesn’t show — but the demand data will — is that crash games punch far above their 1.5% catalog weight when it comes to actual player attention.

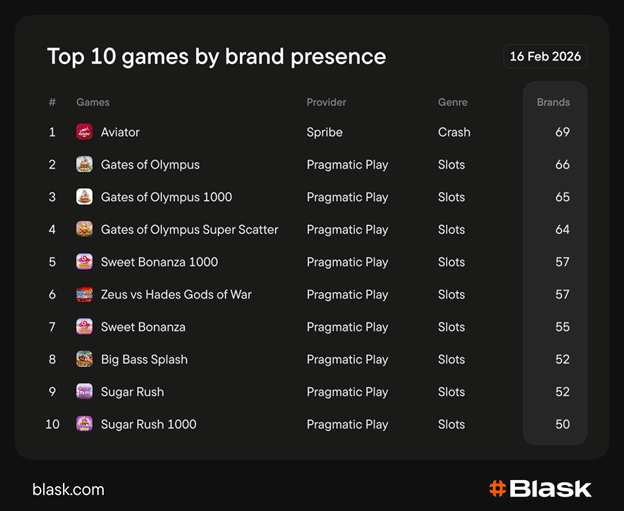

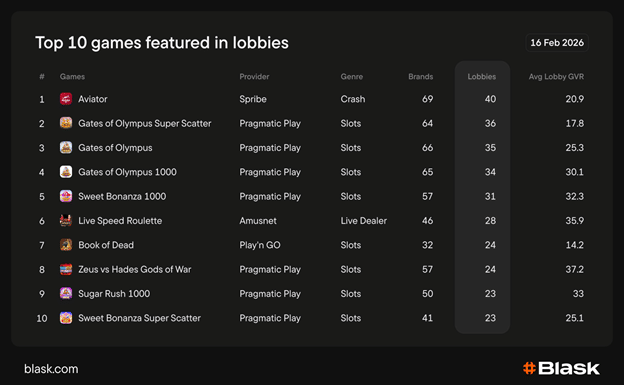

The distribution table: most-carried titles

Pragmatic Play’s dominance is near-total: nine of the top ten most-carried titles belong to the provider, covering three franchise families — Gates of Olympus (three variants), Sweet Bonanza (two), and Sugar Rush (two). Regular Gates of Olympus leads the Pragmatic pack, with its 1000 and Super Scatter variants close behind. Sweet Bonanza 1000 and Zeus vs Hades Gods of War tie at 57 brands, while Sweet Bonanza, Big Bass Splash, Sugar Rush, and Sugar Rush 1000 round out the cluster.

The lone interloper is Spribe’s Aviator, which leads distribution by a small margin. Outside Pragmatic, no other slots provider breaks into the top ten by distribution, revealing just how heavily operators lean on a single supplier for their core shelf.

Who gets the lobby’s hero tiles

Aviator leads by sheer lobby count — more operators feature it on their front page than any other title. But high presence doesn’t mean premium placement: its average GVR sits in the twenties. Contrast that with Book of Dead from Play’n GO, which appears in far fewer lobbies but earns the best average GVR in the entire top ten — operators who do feature it clearly treat it as a top-rail anchor.

Apart from Aviator, another notable crossover breaks the slots monopoly. Live Speed Roulette from Amusnet climbs to sixth in lobby presence despite sitting outside the brand-presence top ten entirely. Meanwhile, Gates of Olympus Super Scatter earns the tightest GVR among the Pragmatic titles, signaling that the newest variant in the franchise gets premium shelf positioning while older siblings drift toward mid-shelf.

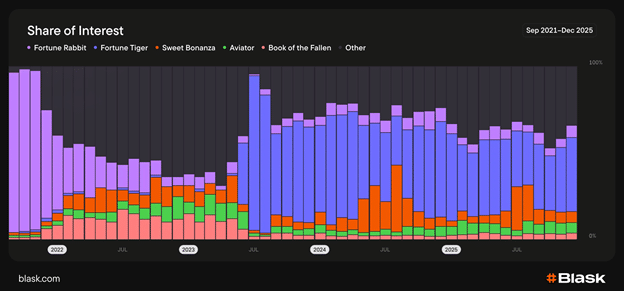

Historical share of interest: four years of demand evolution

The historical Share of Interest chart spanning 2022 through early 2026 reveals two distinct eras in Nigerian player attention.

The Fortune Rabbit era (2021–2022). In late 2021, PG Soft’s Fortune Rabbit held a near-monopoly on player attention, commanding over 90% of total player interest. Through 2022, that grip loosened considerably as Sweet Bonanza and Book of the Fallen carved out growing shares and the “Other” category expanded.

The Fortune Tiger takeover (mid-2023–early 2026). Fortune Tiger burst onto the scene around mid-2023, rapidly seizing the dominant position. Over the following year and a half its share gradually eroded as the “Other” segment expanded, but the game never lost its grip entirely. As of early 2026, Fortune Tiger still commands roughly a third of all search-driven player interest in the country.

Share of interest — current snapshot (February 2026)

The supply-demand gap in Nigeria is enormous. Fortune Rabbit and Fortune Tiger jointly command two thirds of all player interest, yet neither game appears anywhere in the top-ten brand presence or lobby presence rankings. PG Soft’s titles are the demand story, Pragmatic Play’s franchise is the supply story. Operators stock and promote Pragmatic Play across their shelves, but player interest overwhelmingly gravitates to PG Soft’s Fortune series.

The top five titles account for roughly 78.7% of total interest, with Sweet Bonanza, Aviator, and Book of the Fallen filling out the podium behind the Fortune series duopoly. Crash games punch above their 1.5% catalog share: Aviator and JetX together claim over 5% of interest. Crown Coins from Endorphina is the breakout dark horse, up 142.9% year-on-year.

Yet beneath the headline numbers, a structural shift is underway: all three leading slots — Fortune Rabbit, Fortune Tiger, and Sweet Bonanza — are losing share year-on-year, suggesting the market is slowly redistributing attention away from its legacy anchors and toward a broader set of titles.

The bigger picture

Nigeria’s casino shelf tells two parallel stories. The supply side is a Pragmatic Play monoculture — nine of the top ten distributed titles, seven of ten lobby features — reflecting the provider’s unmatched operator relationships and integration footprint. The demand side belongs to PG Soft’s Fortune series, which captures two-thirds of measured player interest despite significantly lower lobby visibility than the Pragmatic titles that dominate the shelf. The year-on-year decline in share for legacy leaders follows a pattern the market has seen before — every dominant title eventually cedes ground, and the attention it sheds tends to coalesce around a new breakout. With the “Other” segment steadily expanding, the conditions are ripe for the next hit to emerge