One Demand Curve, Three Power Structures: iGaming in Nigeria, DRC, and Cameroon

Three Sub-Saharan iGaming markets moving almost in lockstep on the demand side and diverging completely on the market structure.

Nigeria, the Democratic Republic of Congo, and Cameroon moved through 2025 on demand curves so similar they could almost be overlaid. All three followed the same shape: a first-half decline, a reversal around mid-summer, and sustained growth into 2026 with a December spike around AFCON.

But on top of that shared rhythm, the brand structures look nothing alike, three markets moving in sync on demand, yet pulling in completely different directions on who controls them. So what actually happened inside each one? Let’s take a look.

Blask metrics

- Blask Index — real-time measure of market demand volume for iGaming brands in a given country, based on normalized search data.

- BAP (Brand’s Accumulated Power) — a brand’s percentage share of total market demand in a specific country and period.

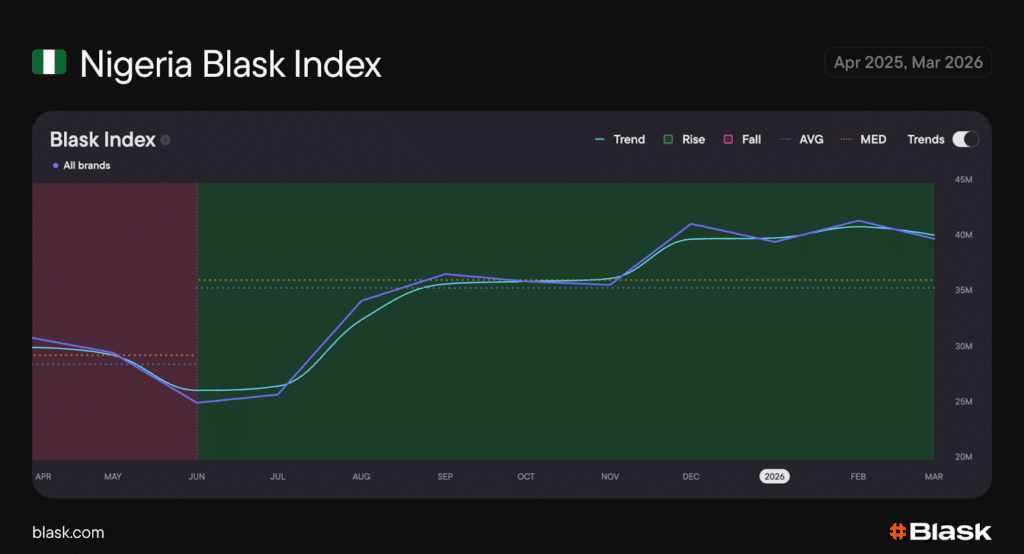

Nigeria, Growth with Competitive Realignment

Nigeria combines scale with acceleration. After a mid-year decline, demand increased sharply from August and reached a higher plateau in Q4.

Demand fell between April and June as the end of EPL and NPFL seasons removed the weekly flow of high-intent betting events. From June onward, the market reset into a sustained growth phase as high-frequency sports content returned. The Premier League restart in August re-established a stable betting cycle, while the FIFA Club World Cup, World Cup qualifiers, and AFCON drove concentrated spikes through H2.

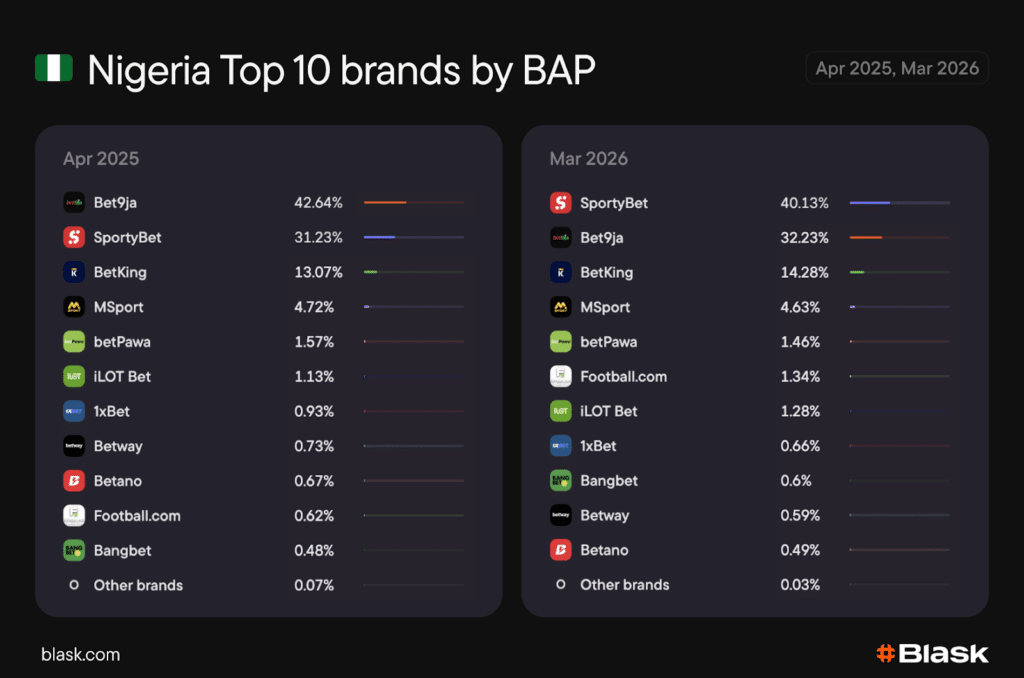

The brand competitive structure shifted at the same time.

In November 2025, SportyBet overtook Bet9ja in BAP and has maintained leadership since. By March 2026, the gap had widened, with SportyBet reaching roughly 40% versus Bet9ja’s 32%, confirming a sustained market shift. Notably, throughout the year BetKing remains the fastest-growing operator, with up to +289% YoY.

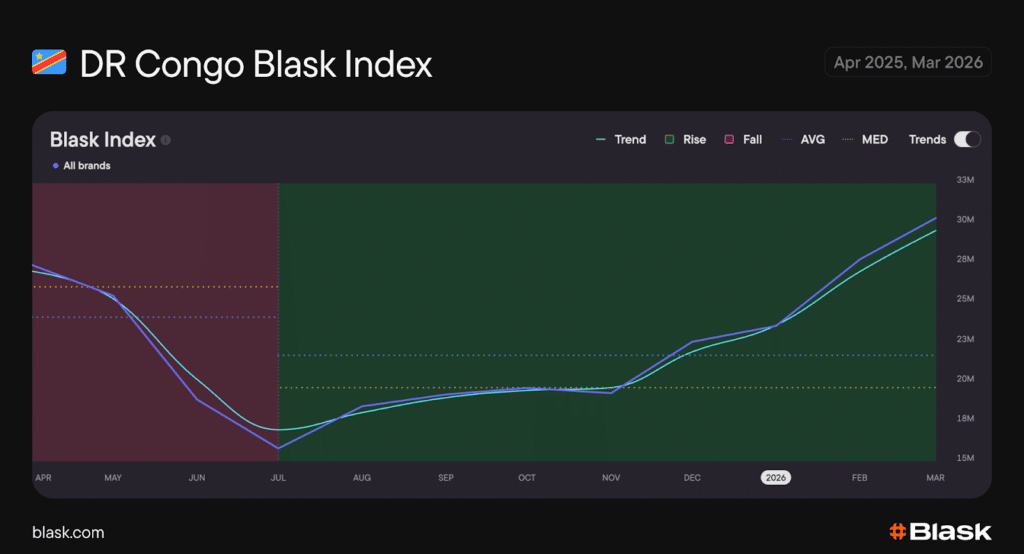

Democratic Republic of Congo, steady growth with a leadership shift

The Democratic Republic of Congo’s demand curve closely mirrors Nigeria’s: a steady decline through the first half of the year, a reversal around mid-summer, and sustained growth into 2026 with a sharp December spike around the AFCON kickoff.

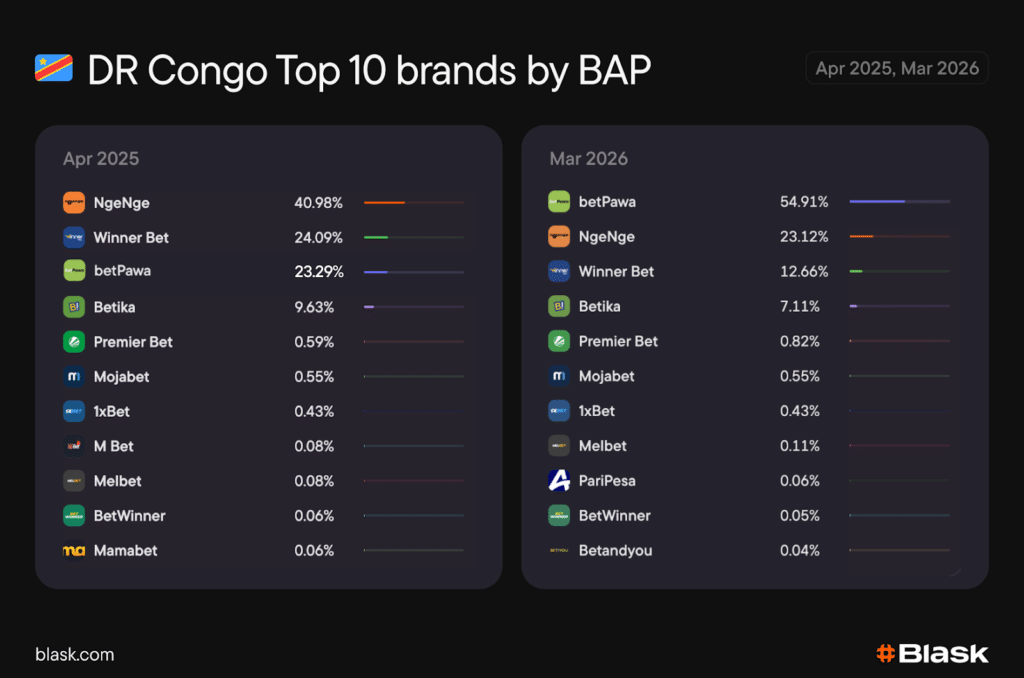

The brand structure saw a sharp reshuffle at the top. betPawa overtook NgeNge to become the new market leader, jumping straight to nearly 55% BAP. NgeNge itself dropped to roughly 23%, giving up close to half of its former share.

Read Also: From Duopoly to Near- Monopoly: SportyBet Surpasses 50% Share in Ghana

Winnerbet slid from second to third and lost about half its BAP; Betika held fourth with a modest decline. Beyond the top four, no operator holds more than 1% of demand.

This is no longer a three-horse race. Over the past year, DRC has consolidated into a clear single-leader market, with betPawa capturing most of the growth and the former leaders compressing behind it.

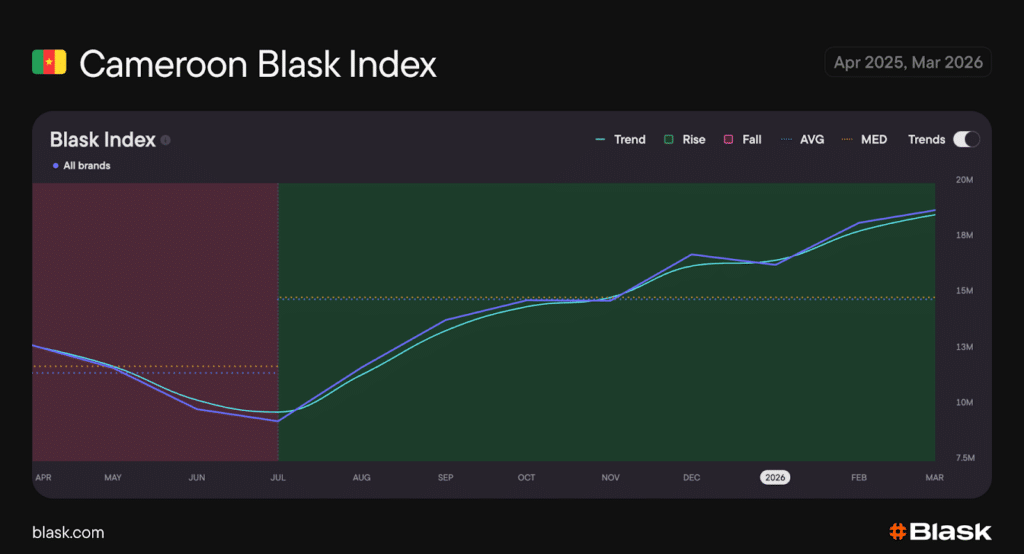

Cameroon, Growth Under Near-Monopoly Conditions

Cameroon follows the same regional pattern: a decline through the first half of the year, a reversal in July, and steady growth through the end of the period, one of the cleanest recovery trajectories in the dataset.

The early-year decline is structurally driven. From March to July, demand decreased almost monotonically, there was no tournament to sustain betting intensity. Short-lived spikes from World Cup qualifiers or the Champions League final were not enough to reverse the trend.

From July onward, the market entered a sustained growth phase as event-driven demand returned: World Cup qualifiers, the AFCON cycle, and major European football restored high-engagement content.

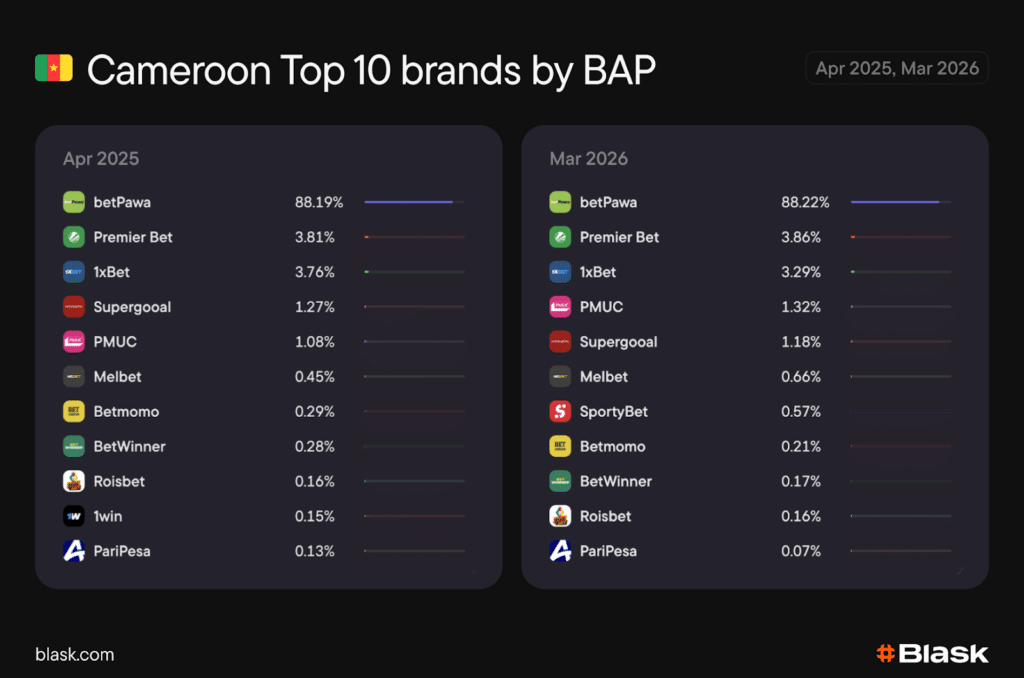

At the brand level, betPawa controls 88.2% of total market demand, effectively turning Cameroon into a single-operator market.

The rest of the field remains marginal. 1xBet briefly crossed the 5% threshold in July 2025, but no challenger has sustained meaningful scale since. Growth reinforces the leader rather than redistributing share, and the market structure leaves minimal room for competitive entry.

Bottom line

On the demand side, these three markets look nearly identical: same calendar, same dip, same recovery, same December peak. The competitive outcomes could hardly be further apart, ranging from a genuine leadership change in a still-contested field, to a full collapse of the old order into a new single-leader structure, to no movement at all as growth simply reinforced the existing leader.

Demand trends in Sub-Saharan Africa increasingly move together. Market structures sharply differ country by country.