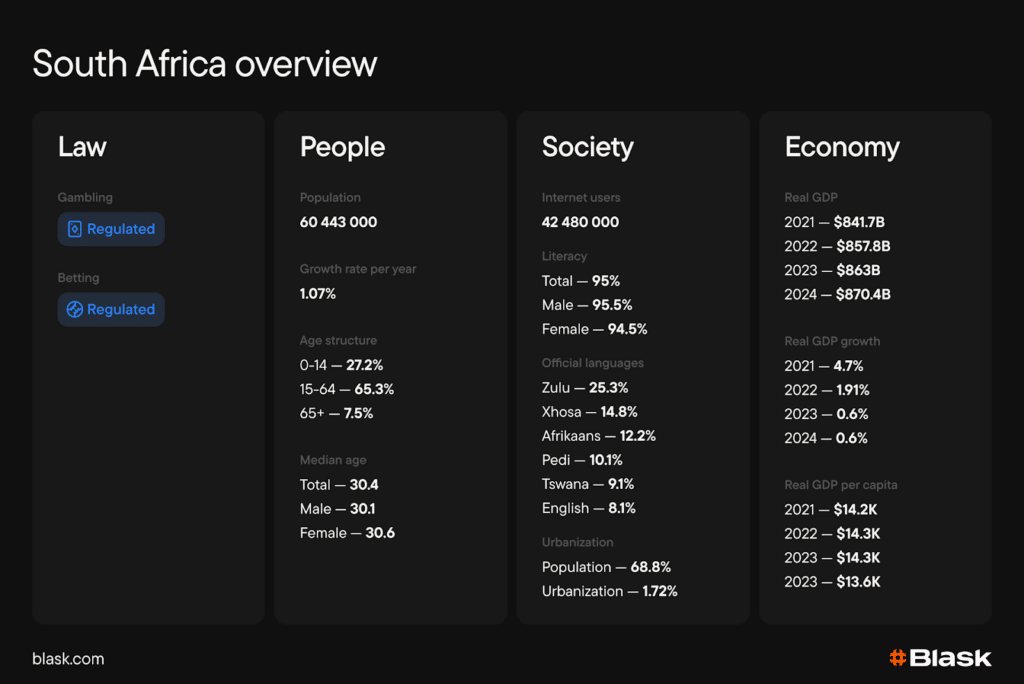

South Africa is a well-established regulated iGaming market with deep roots in the African iGaming landscape. As of early 2026, the market includes 273 active brands, generating an estimated $2.3B CEB. Market momentum remains strong, with +22% year-over-year growth and +7.2% month-over-month expansion as of February 2026.

The defining story of South Africa’s iGaming sector is consolidation within a mature regulated framework. Unlike emerging African markets that are still experiencing early-stage growth or regulatory resets, South Africa operates under a long-standing licensing structure. As a result, the market has moved into an efficiency era where brand strength and acquisition capability determine success.

Blask metrics overview

- Blask Index — real-time measure of market demand volume for iGaming brands in a given country, based on normalized search data.

- BAP (Brand’s Accumulated Power) — a brand’s percentage share of total market demand in a specific country and period.

- CEB (Competitive Earning Baseline) — projected revenue a brand should realistically capture given its market presence, expressed in USD as a min/avg/max range.

Macroeconomic context: population, language, and digital access

South Africa’s population of 60.4 million is growing at 1.07% annually, with ~70% internet penetration and a similar urbanization rate. More than 65% of citizens are working-age adults, and the median age sits just above 30, placing most of the population within the demographics most active in digital entertainment. Literacy reaches 95%, one of the highest rates on the continent, meaning the barrier to engaging with digital products is low across the population.

The country’s linguistic landscape adds a layer of complexity. South Africa has six languages spoken by more than 8% of the population, with four languages outpacing English. Most iGaming platforms default to English, leaving significant room for operators willing to invest in vernacular localization.

South Africa offers a young, growing, digitally literate population with untapped localization potential.

Regulation & taxes: the rules of the game

South Africa’s gambling sector operates under a decentralized but long-established regulatory framework built around provincial licensing authorities.

Regulatory timeline:

- 1996 — National Gambling Act establishes the National Gambling Board and legalizes regulated gambling activity under provincial oversight.

- 2004 — Updated National Gambling Act expands the framework and clarifies the roles of provincial regulators.

- 2008 — National Gambling Amendment Act attempts to create a national online gambling licensing regime. However, implementation stalls and the market continues operating under provincial licensing structures.

- 2024 — Remote Gambling Bill introduced in Parliament to regulate iGaming nationally (stalled by early 2026).

- October 2025 — Landmark Supreme Court of Appeal bans bookmakers from offering fixed-odds bets on casino games (for example, roulette, slots).

- Late 2025–2026 — National Treasury proposes 20% national GGR tax on online gambling (under review as of March 2026).

South Africa’s iGaming market remains restricted under the National Gambling Act 2004, which prohibits interactive gambling (online casinos, slots, roulette, blackjack, live-dealer games) at the federal level. Online sports betting and fixed-odds betting are permitted via provincially licensed bookmakers, but a 2025 Supreme Court of Appeal ruling banned bookmakers from offering casino-style games, even as “fixed-odds“.

Read Also: Blask Wins Best AI Solution at SiGMA Eurasia Awards 2025

Tax stack for operators: Provincial GGR taxes average 6–9%, plus 15% VAT. A proposed 20% national GGR tax on online gambling (introduced late 2025 by National Treasury) would layer on top, pushing the effective burden to 26–29% (or higher with VAT).

Licensing costs:

- Western Cape (most flexible/popular) — application fee ZAR 15,000 (~$900), annual licence ZAR 3,000 (~$180), plus probity/investigation ZAR 12,000 (~$720).

- Other provinces (e.g., Mpumalanga, Gauteng) range ZAR 10,000–20,000 (~$600–$1200) application + ZAR 3,000–15,000 (~$180–$900) annual; additional legal/compliance costs apply.

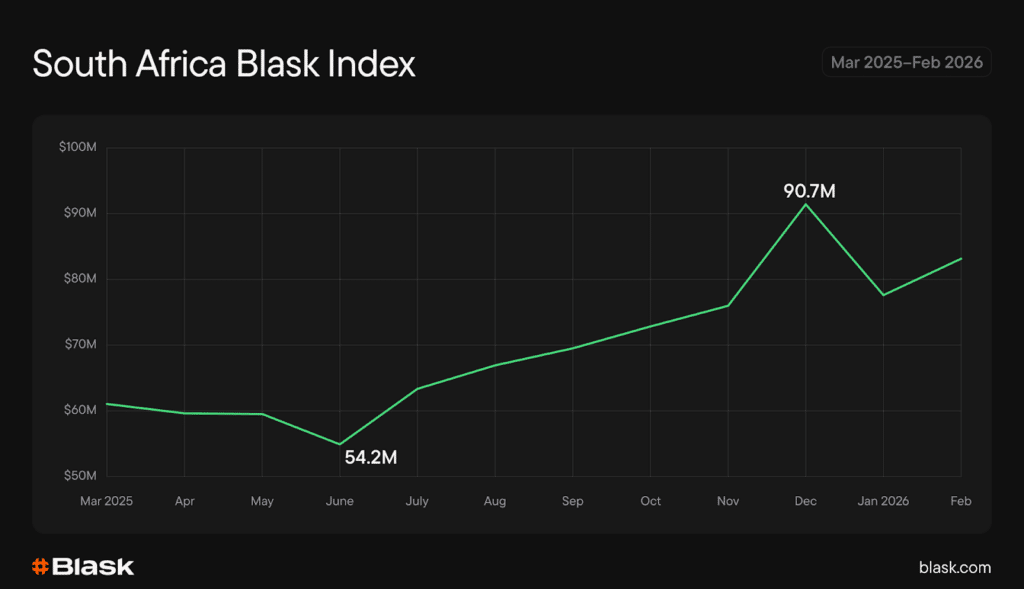

Market dynamics: the seasonal arc

Blask Index followed a clear seasonal arc. The market bottomed in June as European football leagues entered off-season, then climbed steadily through the second half of the year.

Market demand peaked in December, when English Premier League and Champions League fixture density overlapped with holiday spending. A brief January correction was followed by a February rebound, suggesting the market has settled at a higher baseline than last year.

Three phases stand out:

- Mar–May: Soft fade. Market attention eased despite a packed European football calendar — a recurring pattern in South Africa’s seasonal cycle.

- Jun–Oct: Recovery build. The 2025/26 football season launch reversed the slide, with each month adding momentum.

- Nov–Dec: Seasonal peak. Fixture congestion and year-end consumer spending pushed demand to its highest point of the period.

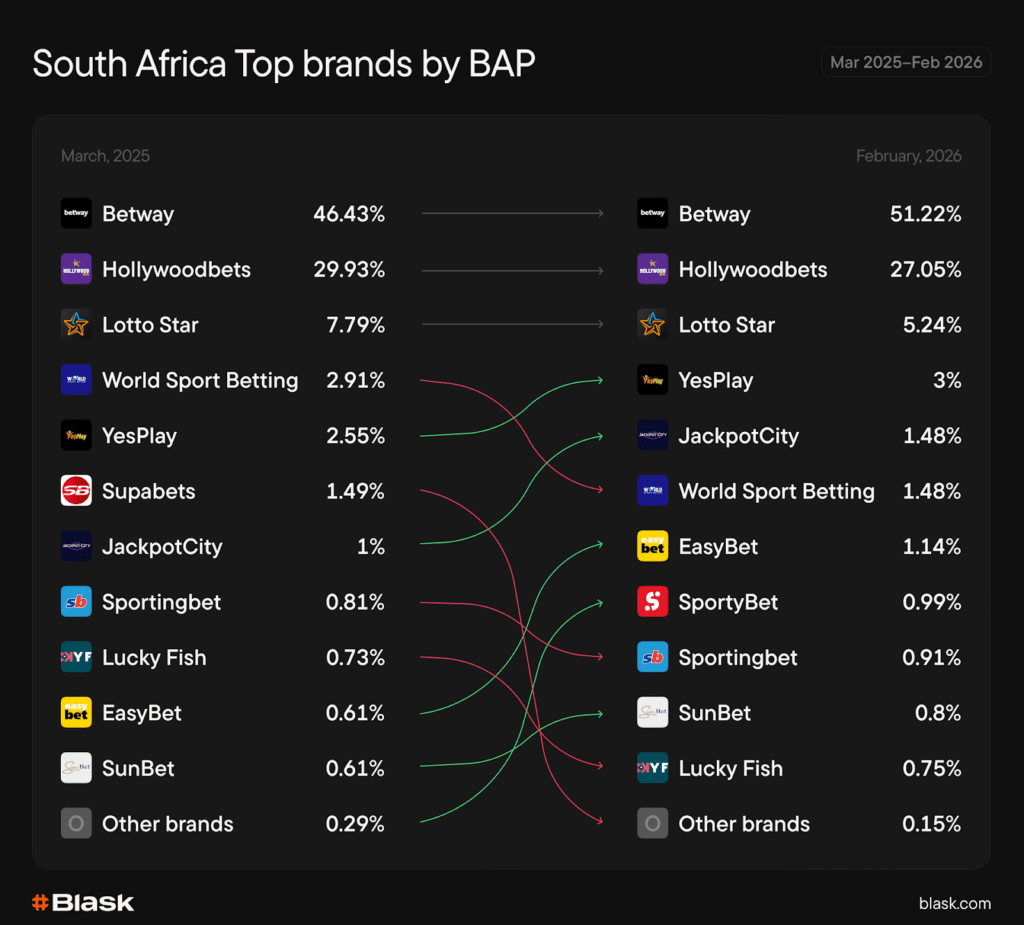

Competitive landscape: two giants

South Africa’s iGaming market is highly concentrated despite the large number of operators. Two brands dominate the competitive hierarchy: Betway and Hollywoodbets.

In March 2025, Betway and Hollywoodbets together controlled more than three-quarters of the market’s demand. By February 2026, the gap between them had widened: Betway gained +4.8 pp, while Hollywoodbets lost 2.9 pp, settling at roughly 27%.

This shift reinforces a key structural trend: the leading operator continues to consolidate power while the long tail fragments.

The rest of the competitive field consists of a mixture of regional betting brands and smaller digital platforms. Operators such as Lotto Star, YesPlay, JackpotCity, and World Sport Betting occupy mid-tier positions but remain far behind the two dominant leaders.

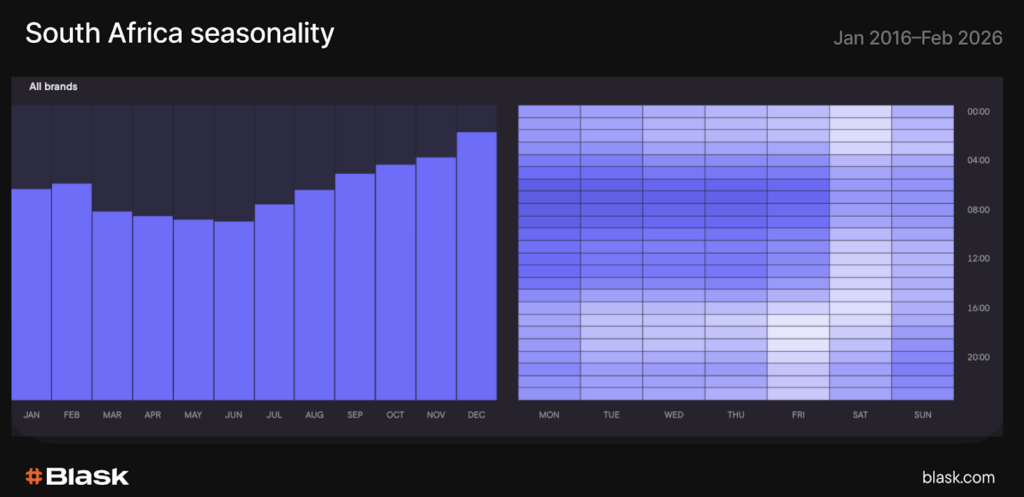

Seasonality & timing: macro cycles and micro peaks

Seasonality patterns reveal a clear year-end demand peak. Market activity strengthens progressively from mid-year into the final quarter, with October through December representing the most active months. This pattern aligns with both international football seasons and holiday spending cycles.

Weekly patterns show Friday evening and Saturday as the most active engagement windows. Activity typically intensifies during late-evening hours when sporting events occur and users have the most leisure time.

These rhythms reflect a familiar structure across sports-driven gambling markets: football calendars create the macro cycle, while weekend leisure patterns concentrate engagement within specific hours.

Bottom line

South Africa represents one of the most mature and structurally stable iGaming markets in Africa. Demand patterns are predictable, the competitive hierarchy is entrenched, and the licensing infrastructure has been in place for decades.

But the ground is shifting. The proposed 20% national GGR tax would push the effective operator burden past 26–29%, while the Supreme Court of Appeal’s ban on fixed-odds casino products has already closed a key revenue diversification channel. Together, these moves could squeeze smaller operators out and accelerate the consolidation trend that already defines the market.

South Africa remains Africa’s benchmark iGaming market — but the regulatory decisions ahead will determine whether that status holds.