Blask data reveals the real size and structure of the Egyptian iGaming market.

Egypt is the continent’s largest unregulated iGaming market in terms of projected revenue. With a population exceeding 111 million young, mobile-connected, and growing every active operator there runs offshore. Yet demand is rising, the hierarchy is clear, and two brands dominate player attention.

Blask metrics overview

- Blask Index — real-time measure of market demand volume for iGaming brands in a given country, based on normalized search data.

- BAP (Brand’s Accumulated Power) — a brand’s percentage share of total market demand in a specific country and period.

- APS (Acquisition Power Score) — benchmark of how many new customers a brand should be attracting given its current market presence, expressed as a min/avg/max range.

- CEB (Competitive Earning Baseline) — projected revenue a brand should realistically capture given its market presence, expressed in USD as a min/avg/max range.

Macro snapshot

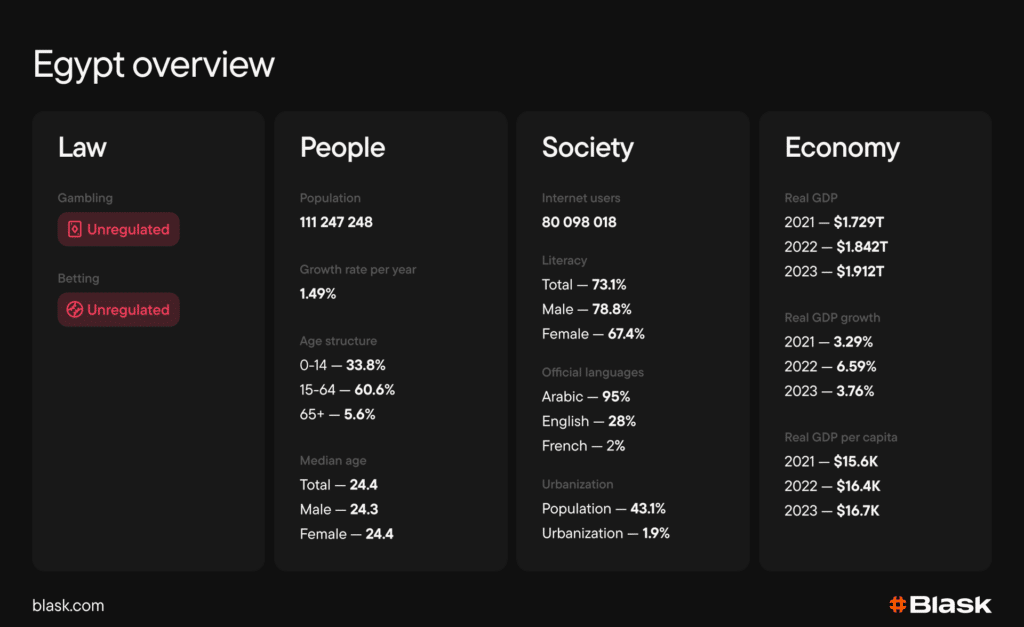

Egypt’s population stands at 111.2 million, with a median age of 24.4, one of the youngest betting demographics on the continent. Internet users number 80.1 million, representing a penetration rate of roughly 72%. Mobile devices dominate web traffic, making smartphone-based betting the default access channel.

Regulation: No framework, no path, no change expected

Egypt’s iGaming market is entirely unregulated. There is no online gambling legislation, no domestic licensing framework, and no regulator with jurisdiction over digital betting. Offshore operators access the market freely — and Egyptian players access them the same way.

Key timeline:

- 1948 — Egyptian Civil Code No. 131 (Articles 739–740) declares gambling contracts void and unenforceable

- 1956 — Law No. 371 prohibits Egyptian nationals from gambling

- 1973 — Law No. 1/1973 permits land-based casinos within four- and five-star hotels, exclusively for foreign nationals; Ministry of Tourism assumes oversight

- 2005 — Agreement between the Egyptian National Post Organization and Greek company Intralot introduces regulated land-based sports betting, open to both locals and tourists

- 2022 — Law No. 8 of 2022 on Hotel and Tourism Entities reaffirms that gambling in designated facilities is restricted to non-Egyptians

Read Also: One Demand Curve: Three Power Structures: iGaming in Nigeria, DRC and Cameroon

iGaming has never been addressed by legislation. No law explicitly prohibits it, and no law licenses it — placing the entire market in a legal gray zone that authorities have shown no urgency to resolve.

Tax stack for operators: There is no tax framework applicable to online operators, no GGR tax, no licensing fee, no formal levy of any kind. Land-based casino operators pay royalties to the Ministry of Tourism of up to 50% of gambling revenues under Law No. 8 of 2022.

Licensing today: No online licensing path exists. The Ministry of Tourism issues land-based casino licenses, restricted to tourist hotels. Zero locally licensed online operators are active in the market. Given entrenched religious and cultural opposition, no regulatory reform is expected in the near term.

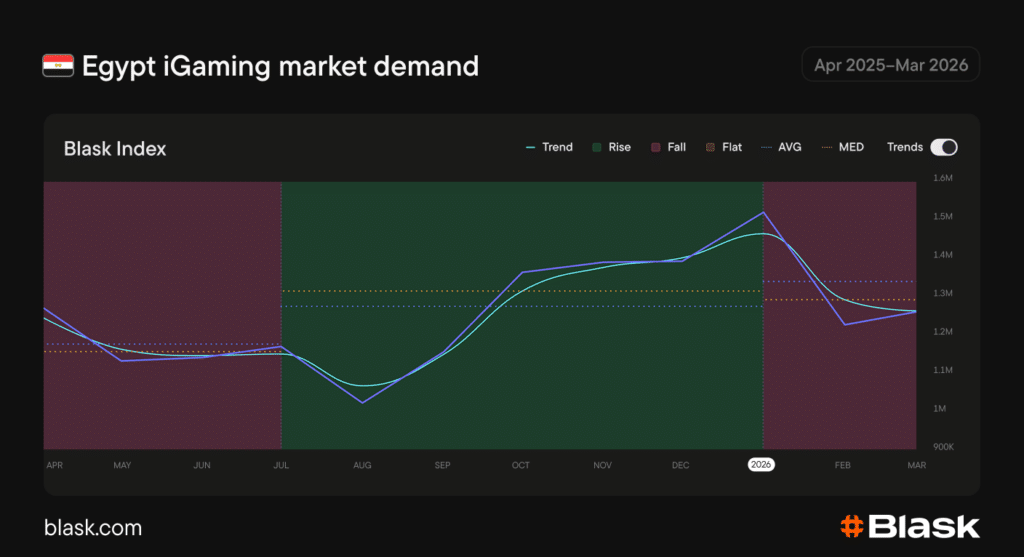

Market dynamics: Gray-market growth on a football engine

Egypt’s iGaming demand follows the European football calendar almost precisely, with a secondary lift from Egypt’s own national team fixtures and AFCON. The twelve-month period from April 2025 through March 2026 breaks into three distinct phases.

Apr–Jul: Summer slide. Demand softened through spring and hit its lowest point in July, as the 2024–2025 European leagues concluded and entered off-season. With no major tournament to sustain betting interest, the market pulled back to its annual floor.

Aug–Nov: Season-launch surge. The return of the English Premier League in August and the Champions League group phase in September drove a sharp recovery. Demand climbed steadily through October and November — the strongest sustained stretch of the period as Egypt’s football-first betting culture locked in around the European fixture calendar.

Read Also: From Duopoly to Near Monopoly: SportyBet Surpasses 50% Demand Share in Ghana

Dec–Mar: AFCON peak, then stabilization. AFCON 2025, hosted in Morocco from December 21 to January 18, delivered an additional spike. Egypt reached the semi-finals before losing to Senegal, sustaining domestic betting interest deep into January. Demand dipped after the tournament concluded, then partially recovered through February and March as European leagues entered their title-run stretch.

Competitive landscape: A two-brand market with a collapsing long tail

Egypt’s competitive structure is among the most concentrated on the continent. 1xBet and Melbet together hold the overwhelming majority of total market demand — a combined dominance that leaves almost no oxygen for the rest of the field. This is not an oligopoly; it is effectively a duopoly with a distant supporting cast.

1xBet has strengthened its position over the twelve-month period, pulling further away from the pack. Melbet, the clear number two, has lost ground. The real movement sits further down: Linebet climbed from fourth to third, displacing 888Starz, which slipped down the rankings. 1win and Stake held relatively steady in the mid-table.

The long tail has effectively ceased to exist “Other brands” account for a negligible share of BAP by March 2026, down from an already minimal starting point. 1xBet’s brand dominance is built on aggressive marketing and deep localisation in Arabic-speaking markets. New entrants are not blocked; they are simply outspent.

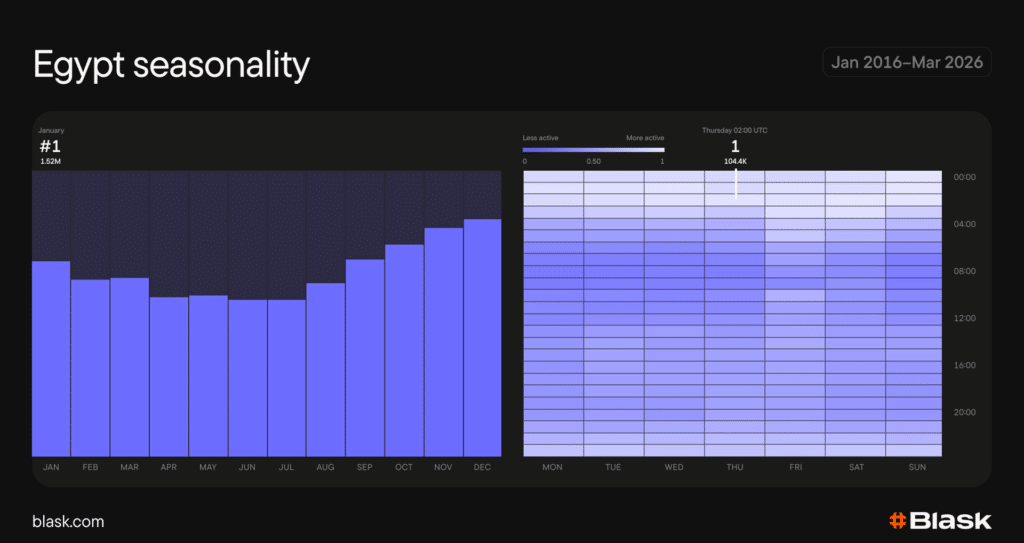

Seasonality: Football-driven, with a clear winter peak

December is the standout month, with demand peaking sharply driven by the convergence of the Premier League’s congested winter schedule and AFCON 2025, which ran from December 21 through January 18. November and January follow close behind. The weakest window runs through May, June, and July, when European leagues enter off-season and no major tournament fills the gap.

The day-by-hour heatmap shows a notably uniform pattern across the week Egypt’s betting activity is spread relatively evenly across all seven days, with no single day dominating the way Saturday does in African markets with stronger accumulator cultures. Activity is concentrated in a daytime-to-evening band, consistent with Cairo local time.

Conclusion

Egypt is one of Africa’s top iGaming markets by revenue unregulated, offshore-driven, and consolidating fast around two dominant brands. That concentration is not a ceiling, the order below the top two is still in motion. In a market with no licensing barrier and no incumbent regulator to navigate, timing and localisation are the only real entry variables.