Tunisia is a market of 12M people where offshore brands have quietly built a functioning iGaming economy around a state monopoly that can no longer keep up. More than ten operators compete for player attention across the April 2025 – March 2026 data period, in a market where demand tracks the football calendar with striking precision.

The single most important thing happening in Tunisia right now is legislation. After years of operating in legal ambiguity, the market is on the verge of a regulatory intervention that will change the rules for every operator currently active.

What makes this moment unusual is that consolidation is already underway without any regulatory trigger. The competitive order is shifting, the long tail is shrinking, and the market is organizing itself ahead of whatever framework the government eventually delivers.

Blask metrics overview

Blask Index — real-time measure of market demand volume for iGaming brands in a given country, based on normalized search data.

BAP (Brand’s Accumulated Power) — a brand’s percentage share of total market demand in a specific country and period.

APS (Acquisition Power Score) — benchmark of how many new customers a brand should be attracting given its current market presence, expressed as a min/avg/max range.

CEB (Competitive Earning Baseline) — projected revenue a brand should realistically capture given its market presence, expressed in USD as a min/avg/max range.

Macro Snapshot

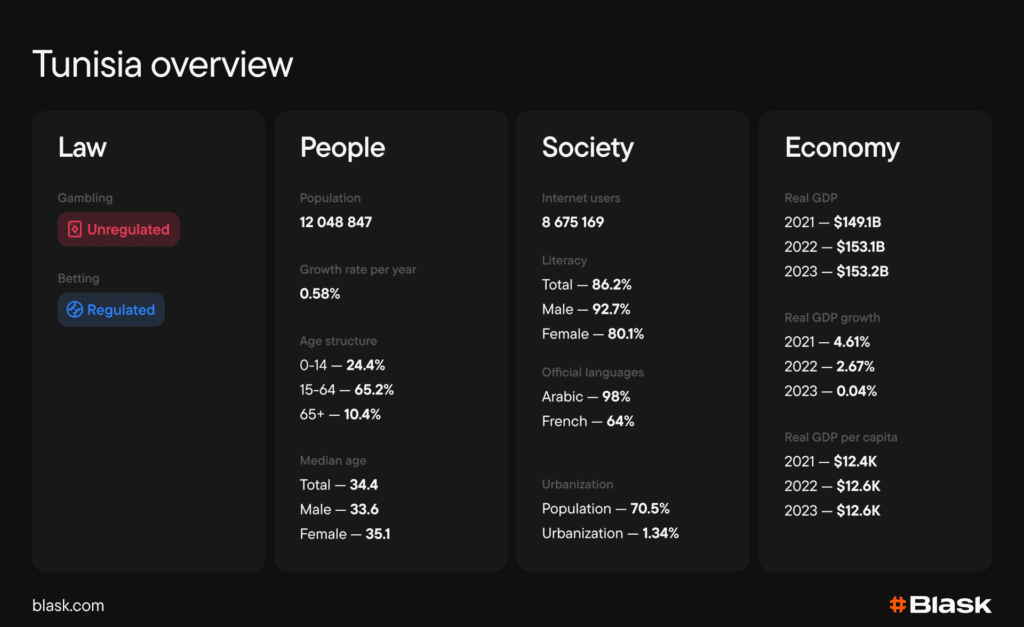

Tunisia’s population stands at 12M, with a median age of 34.4 — a mid-range demographic by regional standards. Internet users number 8.7M, representing a penetration rate of roughly 72%. Mobile connectivity is the dominant access channel, with cellular connections equivalent to 128% of the population.

Regulation: a monopoly under siege, a law stuck in transit

Tunisia’s gambling market is split in two. Land-based casinos require joint authorization from the Ministry of Interior and the Ministry of National Economy under Law No. 74-21 of 1974. Online sports betting sits under Promosport, a state-owned entity holding a statutory monopoly over sports prediction games and lotteries. No licensing framework exists for private online operators — and yet they dominate the market.

Key timeline:

- 1974 — Law No. 74-21 establishes the legal basis for casino operations, requiring ministerial authorization

- 1998 — Advertising Law No. 98-40 introduces general guidelines that indirectly restrict gambling promotion

- 2024 — Minister of Youth and Sports Sadok Mourali announces a draft law covering games of chance, cash betting, and sports betting, following consultations with 26 public institutions including the Central Bank and Competition Council

- 2025 — Revised draft submitted to the Prime Ministry; Council of Ministers review pending

- January 2026 — A group of 23 MPs submits a separate parliamentary proposal targeting online gambling specifically, seeking to revise Decree-Law No. 74-20 of 1974 and expand the definition of gambling to cover digital platforms and mobile apps

Tax stack for operators: A 25% withholding tax applies to gambling and online gambling revenues under Tunisian tax legislation, levied on gross gambling revenue. No additional licensing fee framework exists for online operators — the tax applies in principle, but enforcement against offshore operators is effectively absent.

Licensing today: One path exists — Promosport’s state monopoly — and it is not open to private operators. Zero privately licensed online operators are active in the market. The parliamentary proposal of January 2026 would introduce site-blocking powers, account suspension, and mandatory cooperation from digital service providers, but it has not yet been enacted.

Read Also: Most Valuable Gray Market in Africa According to Blask

Market dynamics: a football engine with a regulatory drumbeat in the background

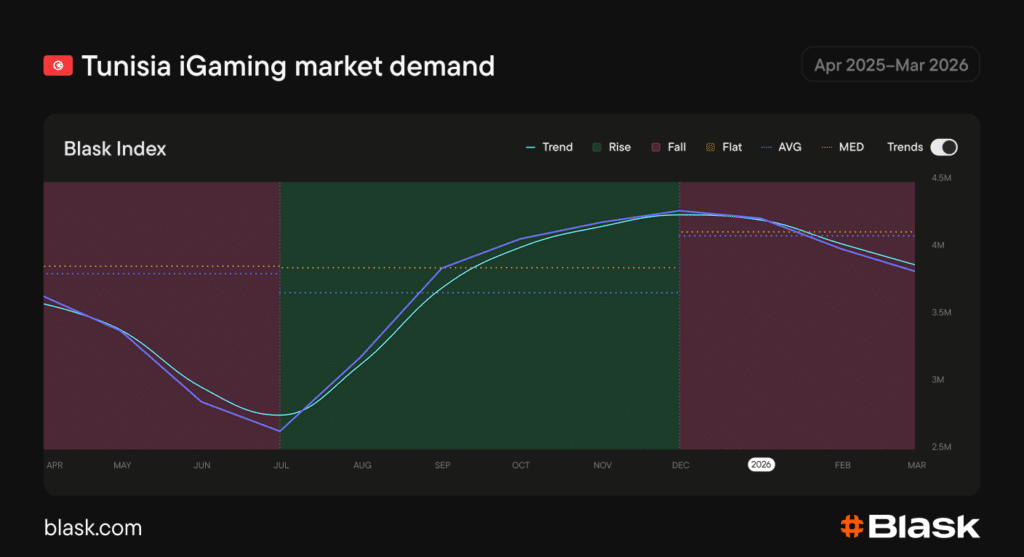

Tunisia’s iGaming demand follows the European football calendar almost exactly, with AFCON providing a secondary seasonal spike. The April 2025–March 2026 period breaks into three distinct phases.

Summer trough (Apr–Jul). Demand fell sharply from April and hit its lowest point in July, as the 2024–25 European leagues concluded and entered off-season. Tunisia qualified for AFCON 2025 but the tournament was still months away, leaving no major fixture anchor to sustain betting interest through the summer.

Season-launch surge (Aug–Nov). The Premier League’s return in August and Champions League group stage in September drove a steady climb through November. Espérance de Tunis’s CAF Champions League campaign added a domestic layer from November onward.

AFCON peak, then stabilization (Dec–Mar). December was the period’s demand peak — AFCON 2025 in Morocco ran December 21 to January 18, with Tunisia exiting in the round of 16 against Mali. Demand softened post-tournament before partially recovering as Espérance reached the CAF Champions League quarter-finals against Al Ahly in March.

Competitive landscape: a stable top, a reshuffling middle

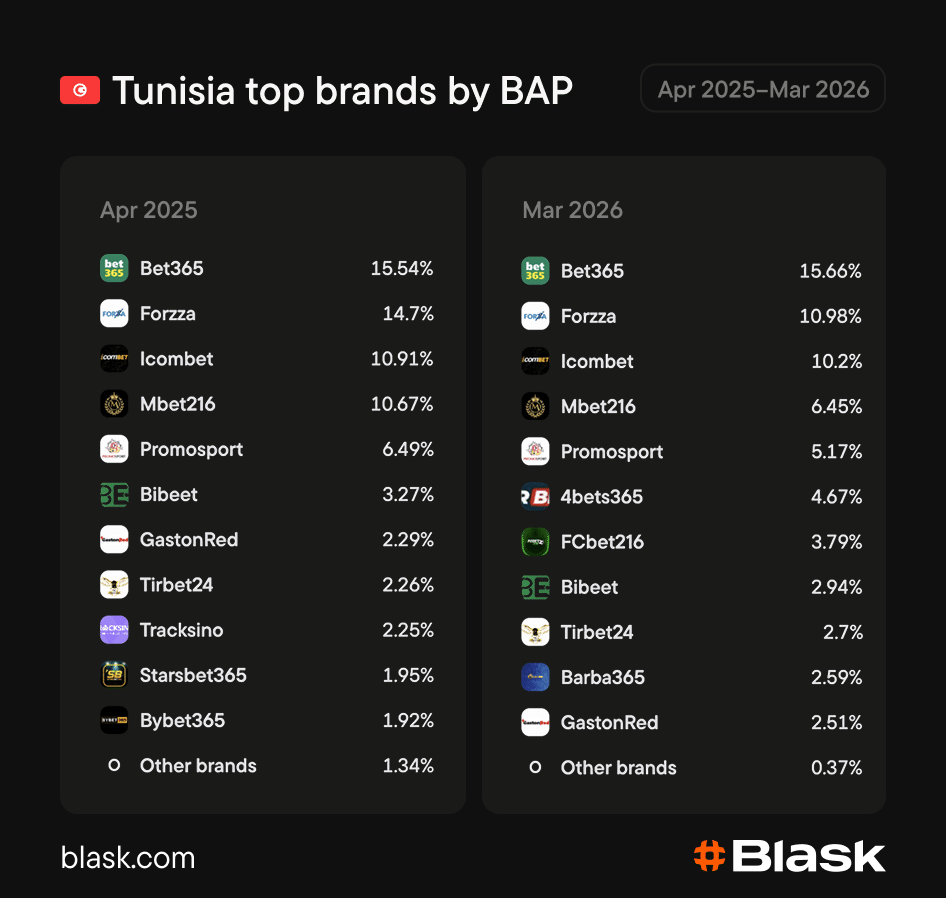

Tunisia’s market is an oligopoly with a clear leader. Bet365 holds the top position at 15.7% BAP — virtually unchanged across the twelve-month period — with Forzza and Icombet occupying second and third. The top three combined account for roughly 37% of total market demand, with no single brand achieving the kind of dominance seen in Egypt’s 1xBet-led market.

The movement is in the middle. Forzza slipped from 14.7% to 11.0% — the sharpest decline among established brands. Mbet216 dropped similarly, from 10.7% to 6.5%. The space they vacated was filled by new entrants: 4bets365 and FCbet216 both entered the top ten by March 2026, claiming 4.7% and 3.8% respectively. Tirbet24 and GastonRed held steady and edged slightly higher.

Promosport — the state monopoly — sits fifth at 5.2% BAP by March 2026, down from 6.5% at the start of the period. A state-sanctioned operator losing ground to offshore brands in its own regulated category is the clearest signal of where Tunisia’s market is heading.

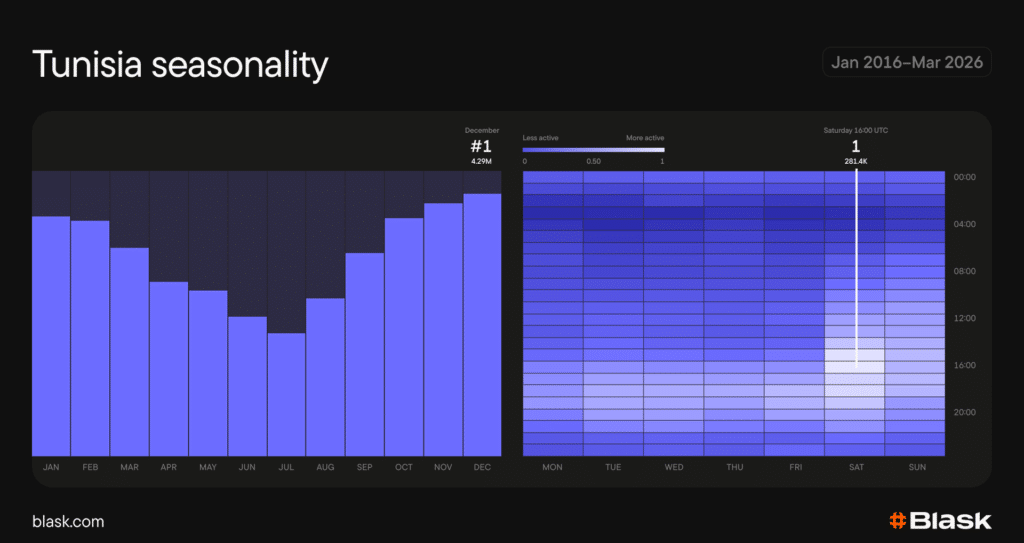

Seasonality: football-driven, with a pronounced winter peak

The weakest window runs from April through July, bottoming in July when European leagues are in off-season. Demand recovers steadily from August, building through November and peaking sharply in December — driven by AFCON 2025 and the Premier League’s congested winter schedule running simultaneously.

The day-by-hour heatmap shows activity concentrated in the afternoon-to-evening band, brightest around 16:00–18:00 local time. Saturday and Sunday register slightly higher than weekdays, consistent with a market oriented around weekend football fixtures. Monday is the quietest day of the week.

Conclusion

Tunisia is a gray market in the final stretch before regulatory intervention. Offshore brands have built a stable, football-driven iGaming economy around a state monopoly that ranks fifth in its own market — and two separate legislative proposals are now in motion simultaneously.

The competitive order is not locked. Forzza and Mbet216 both shed significant share across the period while 4bets365 and FCbet216 entered the top ten from outside it. Movement at that level is available to operators who move early and localise effectively.

When the regulatory framework lands, the market resets. Tunisia rewards operators already embedded when that happens.