North Africa’s iGaming split: two 1xBet markets and one contested field

The same calendar drives all three markets. Only one of them is still genuinely contested.

Egypt, Algeria, and Tunisia moved through 2025 on the same demand curve — quiet summer, autumn recovery, December peak around AFCON in Morocco. But the competitive picture splits cleanly in two: Egypt and Algeria are locked down by a single dominant operator, while Tunisia’s field is still genuinely contested.

Here is how each market played out — what drove the demand curve, who captured it, and where the competitive field is heading.

Blask metrics

Blask Index — real-time measure of market demand volume for iGaming brands in a given country, based on normalized search data.

BAP (Brand’s Accumulated Power) — a brand’s percentage share of total market demand in a specific country and period.

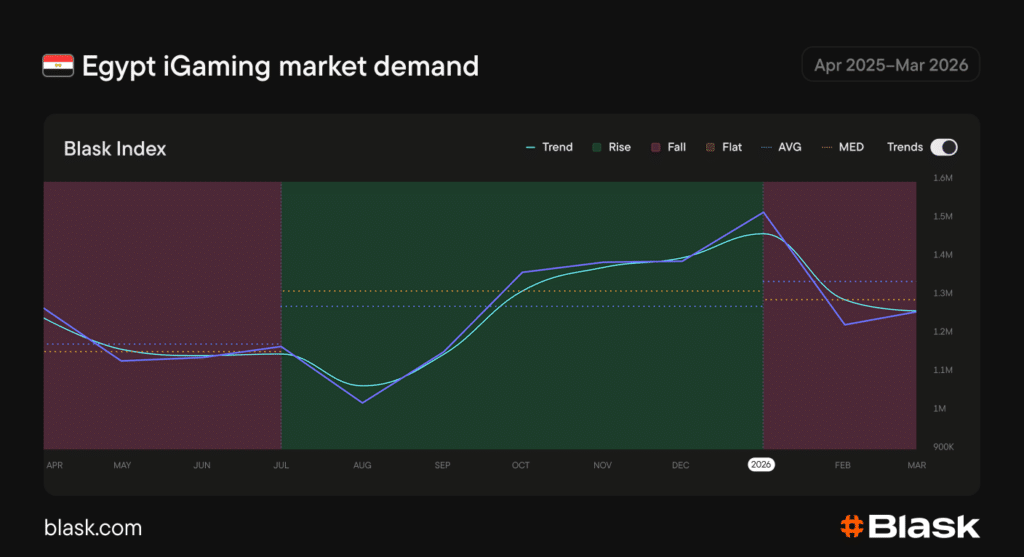

Egypt — a near-monopoly that keeps tightening

Egypt’s demand through the last 12 months followed a clear two-act structure. The first half was quiet — the Egyptian Premier League wrapped up by late May, European football went into its summer break, and with no major tournament to fill the gap, engagement pulled back through July and into August. From August onward, the Premier League’s return re-anchored weekly betting activity, while CAF Champions League fixtures and World Cup qualifiers pushed demand higher through autumn.

December brought the sharpest movement of the year, as AFCON 2025 kicked off in Morocco on December 21 and concentrated national attention around Egypt’s campaign. Once the group stage passed, demand dropped back quickly and settled at a lower level through early 2026.

1xBet entered the period already holding the dominant share of market demand and expanded it further by March 2026. Melbet, the only operator with real scale behind the leader, gave up ground over the year. Linebet was the one exception, growing steadily from a small base. No other operator moved the needle. The market is effectively a one-brand story, with the rest of the field competing for what remains.

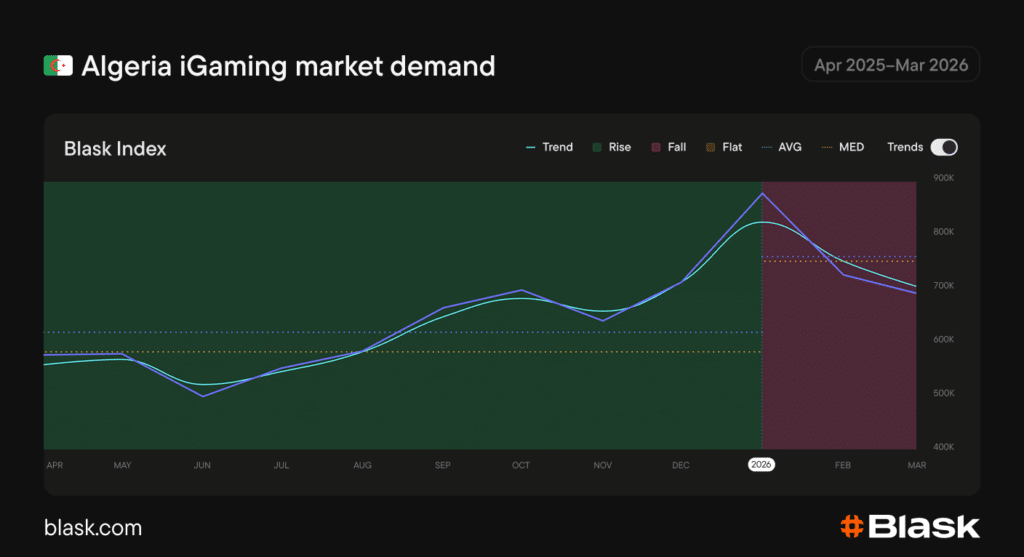

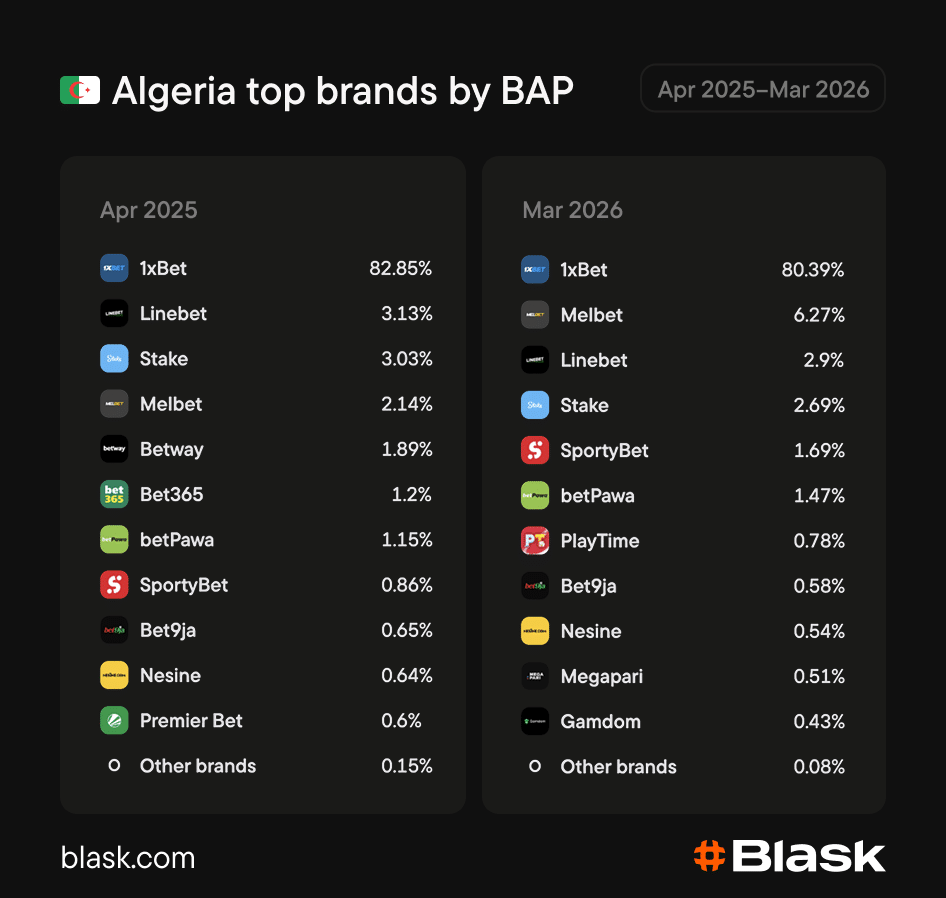

Algeria — 1xbet market

Algeria’s demand curve was the flattest of the three through the first half of 2025. Engagement held relatively steady before dipping modestly around June and July as the Algerian Ligue Professionnelle 1 wound down and European football went quiet.

From August onward, the market climbed consistently. The return of European club football and CAF competitions restored a regular betting calendar, and Algeria’s World Cup qualification campaign added a layer of national engagement that drove demand higher through September and October.

Read Also: Tanzania iGaming market overview: betPawa Near-monolopy

December produced the sharpest movement of the year, as AFCON 2025 in Morocco — a short trip for Algerian fans — opened on December 21 and pulled engagement to its highest point in the period. The correction that followed in January and February was noticeable but left demand well above where it had started the year.

1xBet’s position in Algeria is in a different category from any other market in this dataset. The operator held an overwhelming share of market demand in April 2025 and closed the period barely changed — the market simply did not generate meaningful competitive pressure.

Melbet was the only brand to register real movement, more than doubling its share over the year, largely absorbing the space left by Betway and Bet365, both of which dropped out of the top rankings entirely. SportyBet and betPawa edged up from negligible bases. Beyond that, movement was marginal.

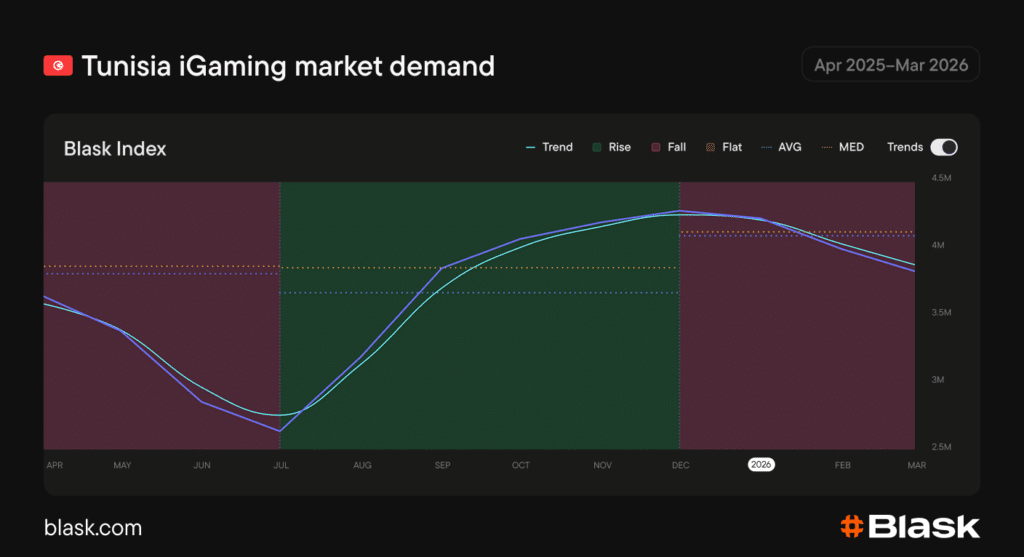

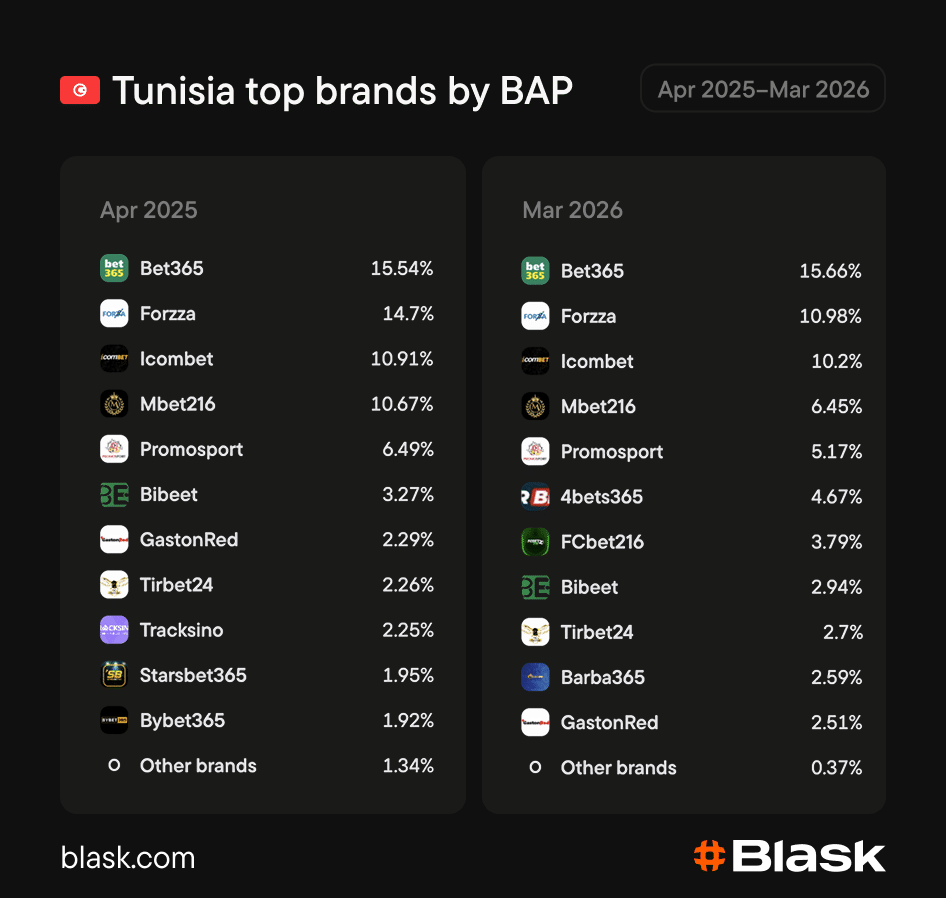

Tunisia — contested and still open

Tunisia’s demand curve was the smoothest of the three markets — a gradual decline through the first half of the year as the Tunisian Ligue Professionnelle 1 wound down and European football went quiet, followed by a steady climb from July that built consistently into December.

Tunisia’s World Cup qualification, sealed in September 2025 with a dramatic late winner over Equatorial Guinea, added a strong layer of national engagement through the autumn months. AFCON 2025 in Morocco drove the December peak, with Tunisia participating in the tournament before being eliminated by Mali in the round of sixteen.

Unlike Egypt and Algeria, the pullback from January onward was gradual rather than sharp, and demand held at a relatively high floor through early 2026 — the most stable exit trajectory of the three markets.

The brand landscape is where Tunisia separates itself completely from the other two. No operator comes close to dominance — the top of the market is genuinely clustered, with Bet365 holding a narrow lead and Forzza, Icombet, and Mbet216 sitting close behind.

The bigger story is movement within that cluster: Mbet216 and Promosport both lost ground over the year, while newer entrants like 4bets365 and FCbet216 appeared and picked up meaningful share. Tunisia is the only market in this group where the competitive picture is still being actively written.

Bottom Line

All three markets followed the same demand calendar through 2025 — a mid-year dip, a second-half recovery, and a December peak driven by AFCON in Morocco. Where they diverge is in who captured that demand and how securely.

Egypt and Algeria are 1xBet markets — the operator holds a dominant position in both, and any growth in demand flows almost entirely to it. Tunisia runs on a different logic: no 1xBet dominance, a tightly clustered top, and challengers actively gaining share. In Arabic African iGaming, the calendar is shared; the competitive outcomes are not.