Tanzania iGaming market overview: betPawa Near-monolopy

Tanzania is East Africa’s quiet giant. The infrastructure is there, the regulation is solid, and the audience is growing fast.

One operator has effectively won the market. betPawa leads both user demand and projected revenue by a margin without close parallel on the continent, and extended it further across the data period.

What remains is a genuine race for everything beneath it, where global names are losing ground to a fast-rising regional challenger. For operators willing to compete, Tanzania still has room, just not at the summit.

Blask metrics overview

- Blask Index — real-time measure of market demand volume for iGaming brands in a given country, based on normalized search data.

- BAP (Brand’s Accumulated Power) — a brand’s percentage share of total market demand in a specific country and period.

Macro snapshot

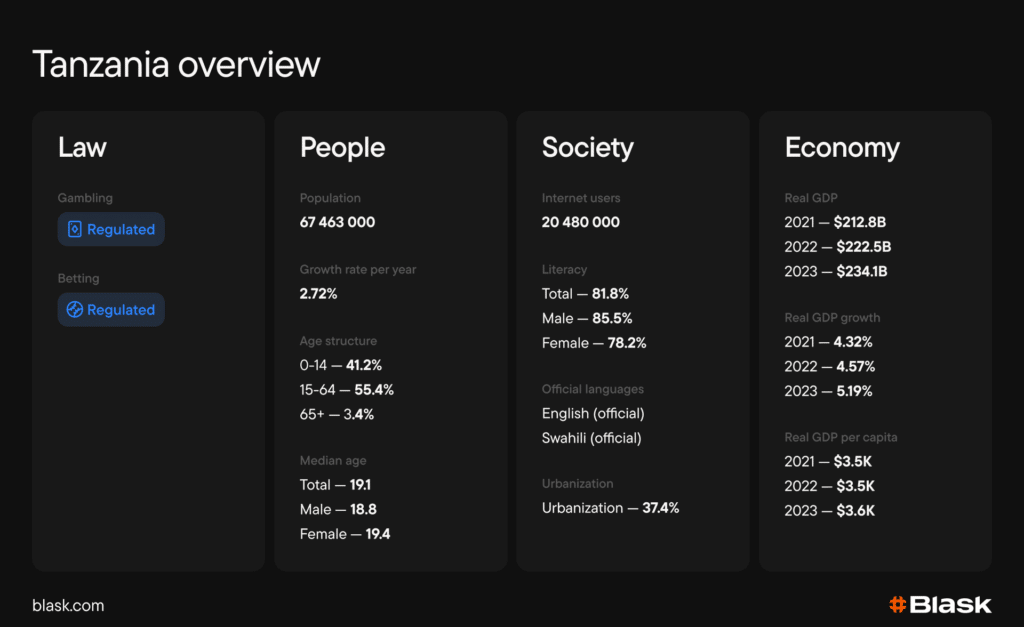

Tanzania’s population stands at 67.46 million, with a median age of 19.1, one of the youngest markets on the continent. Internet users number 20.48 million, representing a penetration rate of around 30%. Mobile devices are the dominant access channel, accounting for the vast majority of web traffic, smartphone-based betting is how Tanzania plays.

Regulation: open market, tightening grip

Tanzania’s iGaming market is fully regulated and open to both local and foreign operators. The Gaming Board of Tanzania (GBT) serves as the sole regulatory authority, overseeing everything from sports betting and online casinos to lotteries and virtual games. The framework is functional and has been in continuous evolution — the current direction is more licensing, more enforcement, and less tolerance for unlicensed operations.

Key timeline:

- July 1, 2003 — Gaming Act (Cap. 41) comes into effect, establishing the GBT as the sole regulator for all gaming activities; replaces the Pools and Lotteries Act of 1967

- 2003 — Gaming Regulations (GN No. 385) set operational standards for all licensed operators

- 2016 — Sports Betting Rules introduced, establishing dedicated compliance requirements for online and retail sportsbooks

- July 1, 2018 — Finance Act 2018 (Act No. 4 of 2018) takes effect; raises sports betting tax from 6% on stakes to 25% on GGR as part of the 2018/19 national budget

- January 23, 2019 — Government restricts all gaming advertising across radio and television nationwide

Read Also: From Duopoly to Near-Monopoly: SportyBet Surpasses 50% Demand Share in Ghana

- September 20, 2019 — Gaming Act amended and consolidated as Cap. 41 R.E. 2019 via the Written Laws (Miscellaneous Amendments) No. 6 Act (Act 13 of 2019)

- July 1, 2023 — Finance Act 2023 takes effect; introduces a mandatory requirement for license applicants to have at least 5% of paid-up share capital owned by Tanzanian citizens

- June 2025 — GBT announces plans to issue 14,124 licenses in the fiscal year (845 new and 13,279 renewals across all license categories, including operator, employee, retail and slot route permits), alongside targeted enforcement actions against unlicensed operators

Tax stack

Sports betting and online gaming operators pay 25% on GGR, plus 15% on net player winnings. Land-based casinos pay 18% GGR and 12% on player winnings. Virtual games are taxed at 10% GGR. Five percent of all gaming tax collected is ring-fenced for Tanzania’s Sports Development Fund.

Licensing process

Licensing runs through a single path, the GBT. Separate licenses are required for online and land-based operations. Foreign companies must meet a minimum capital requirement of $500,000; local companies, $300,000. Online sports betting licenses carry a fee of $30,000; online casino licenses, $40,000. All licenses are valid for one year and must be renewed annually.

Market dynamics: football drives the calendar

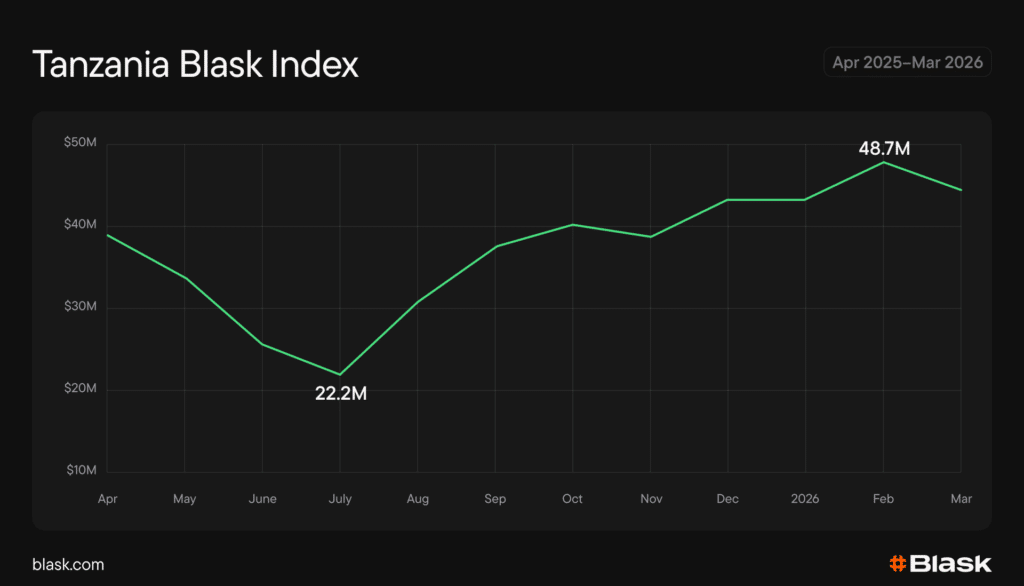

Tanzania’s Blask Index for the April 2025–March 2026 period follows a pattern common across East Africa, shaped almost entirely by the European football calendar. Three distinct phases define the year.

April–July: off-season slide. Demand held relatively stable through the final weeks of the 2024/25 Premier League season, which concluded on May 25, 2025. Once European leagues entered the summer break, the market pulled back sharply, the weakest stretch of the entire data period. With no major club football to sustain accumulator betting culture, the trough bottomed out around July before stabilising.

August–September: season relaunch. The return of club football reversed the decline quickly. The 2025/26 Premier League kicked off on August 15, and the Champions League opened on September 16, bringing simultaneous midweek and weekend fixtures that pushed demand back above its annual average within weeks.

Read Also: One Demand Curve, Three Power Structures: iGaming in Nigeria, DRC, and Cameroon

October–February: sustained elevation. The market held at its highest levels through the final months of 2025 and into early 2026. The full Champions League schedule, running through its league phase conclusion on January 28, 2026, combined with a packed Premier League programme to keep betting volumes consistently elevated.

The window also overlapped with AFCON 2025, hosted by Morocco from December 21 to January 18, where Tanzania’s Taifa Stars reached the round of 16 before falling to the host nation.

Competitive landscape: one brand dominates, one rises fast

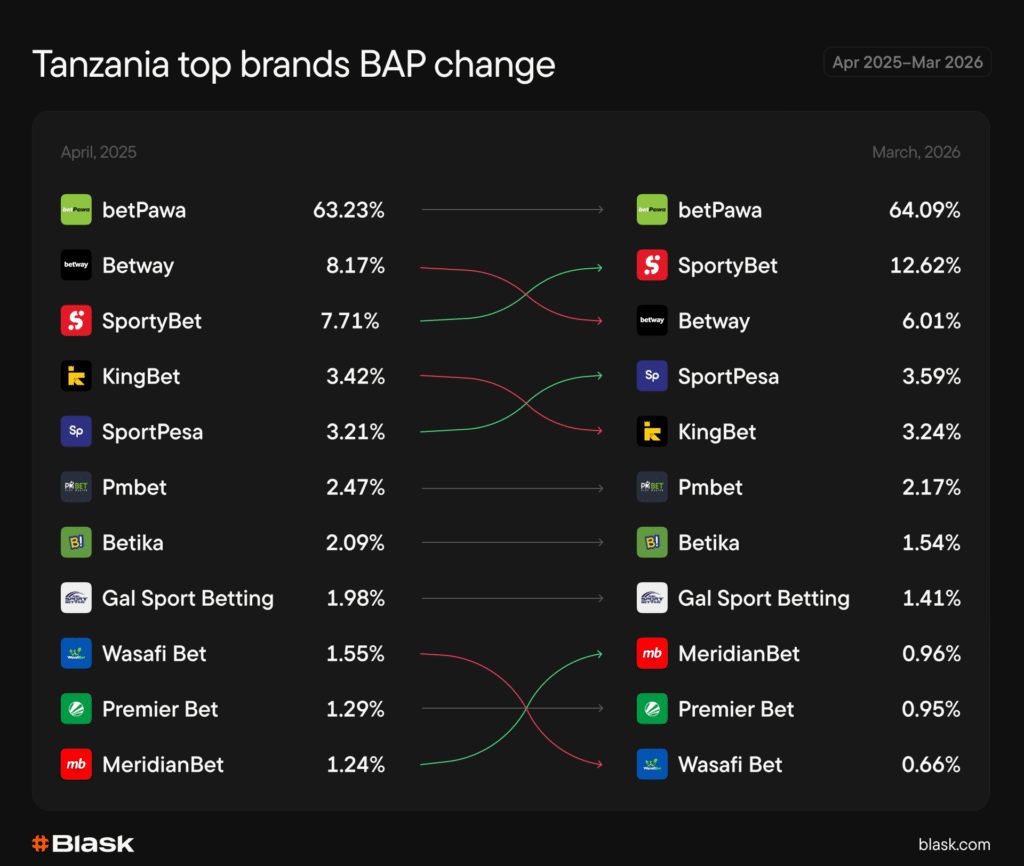

Tanzania’s market is structurally unlike most in Africa. A single operator, betPawa, commands nearly two-thirds of total market demand, a share that grew further across the data period and shows no sign of meaningful erosion. Below it, the combined BAP of every other brand in the top ten doesn’t come close to matching the leader.

The most significant movement in the period belongs to SportyBet, which posted the sharpest rise of any brand in the ranking, climbing from third to second place and growing its BAP by roughly two-thirds between April 2025 and March 2026. That ascent came directly at Betway‘s expense. The globally recognised brand, which opened the period in second position, shed a significant portion of its share and slipped to third.

All brands that appeared in the top rankings across the data period hold GBT licenses. Blask tracks just 42 active brands in the country, a notably thin field, and the long tail is negligible: operators outside the top ten account for a small share of total demand.

For new entrants, the barrier is not regulatory, obtaining a license is achievable. The challenge is competitive: breaking into a market where the top positions are held by established, locally embedded operators, and where betPawa’s lead is not merely large but structurally entrenched.

Seasonality: football calendar, weekend peaks

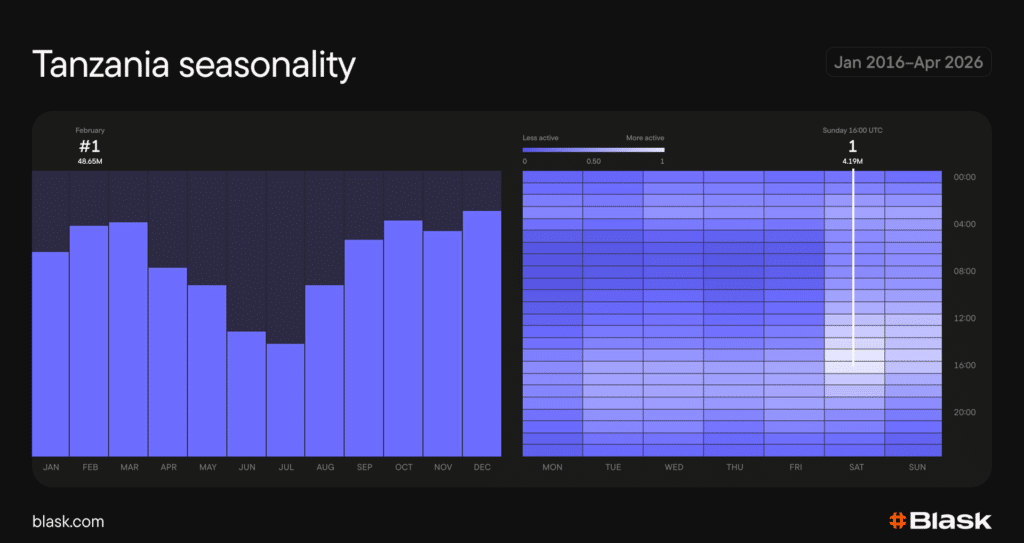

The 2025/26 annual cycle described above is the standard pattern, repeating year after year: a summer trough during the European off-season, a sharp recovery at season relaunch, and sustained highs from autumn through February.

The weekly pattern is equally consistent. Saturday and Sunday dominate the heatmap by a clear margin, driven by Premier League matchdays. The peak activity window sits in the early-to-mid afternoon in East Africa Time, aligning directly with the main Saturday Premier League kickoff slots. Weekday activity is noticeably quieter, picking up only when midweek Champions League fixtures are scheduled.

Conclusion

Tanzania’s iGaming market is defined by a level of concentration rare anywhere on the continent. betPawa holds a dominant share that grew across the entire data period, underpinned by a stable regulatory framework and a football-driven, mobile-first population of nearly 67 million.

That dominance has not frozen the market beneath it. SportyBet’s rise from third to second and Betway’s corresponding retreat, proves that positions can shift, and shift fast. The opportunity in Tanzania is not at the summit. It is in the competitive space below it, where locally committed operators with the right product are still winning ground.

Tanzania rewards operators who embed early, license locally, and build for mobile. The framework is open, the audience is growing, and the race for second place remains open.