Brand demand rules African iGaming: Blask Maturity Index breakdown

Africa runs on brand recognition — and Blask data proves it.

Africa runs almost entirely on brand demand. In every African market Blask tracks, the Maturity Index stays low, players search for operator names rather than game categories, and brand recognition is what drives acquisition. That pattern holds from the continent’s largest markets to its smallest.

The one exception is Sudan, with an MI of 51.08, where category demand edges past brand demand. But Sudan ranks 126th out of 133 countries in the Blask system. It’s one of the smallest markets tracked globally, and the exception does not challenge the broader picture.

What the Maturity Index reveals across Africa is not whether brand demand dominates, it does, but how much category demand has developed alongside it, and where. This breakdown covers five regions, with the top three markets by MI in each.

Maturity Index, the ratio between two demand layers Blask tracks: brand-level search demand, measured by Blask Index, and generic category-level demand, measured by Categories Blask Index. The Maturity Index compares total category-level demand against total brand-level demand within a GEO and maps the result to a scale of 0 to 100, 0 means all brand search, 100 means all category search.

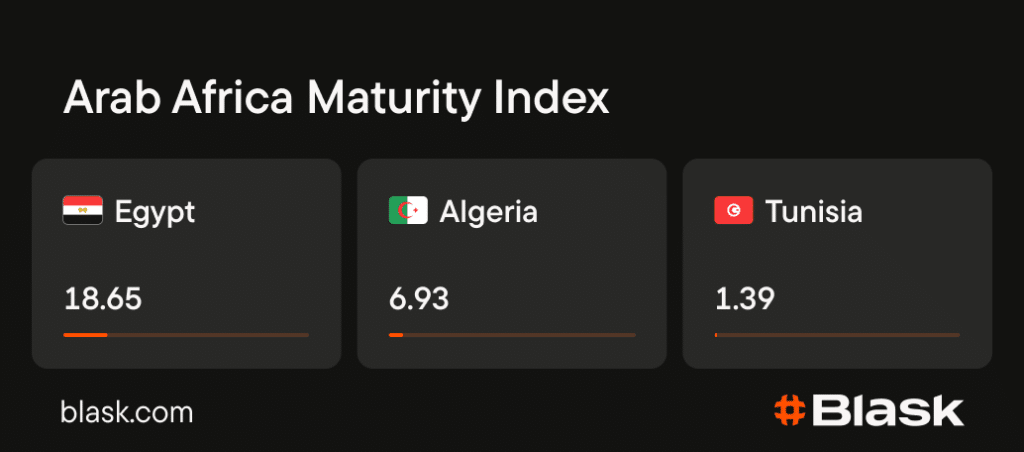

Arab Africa

Arab Africa has the highest category demand on the continent. Egypt leads by a wide margin, its MI has no comparable figure in sub-Saharan Africa. Algeria follows at a distance, and Tunisia sits considerably lower, closer to the continental middle than to its regional peers.

Egypt and Algeria are the only two markets in this dataset where Fantasy outranks Online Betting as the top category. Every other African market in this review is led by Online Betting. The strength of Fantasy demand in Egypt is what separates it from Algeria, and from the continent as a whole.

Tunisia’s MI puts it in a different company from Egypt and Algeria. Online Betting leads there, and the level of category development is more in line with what you see in East or West Africa.

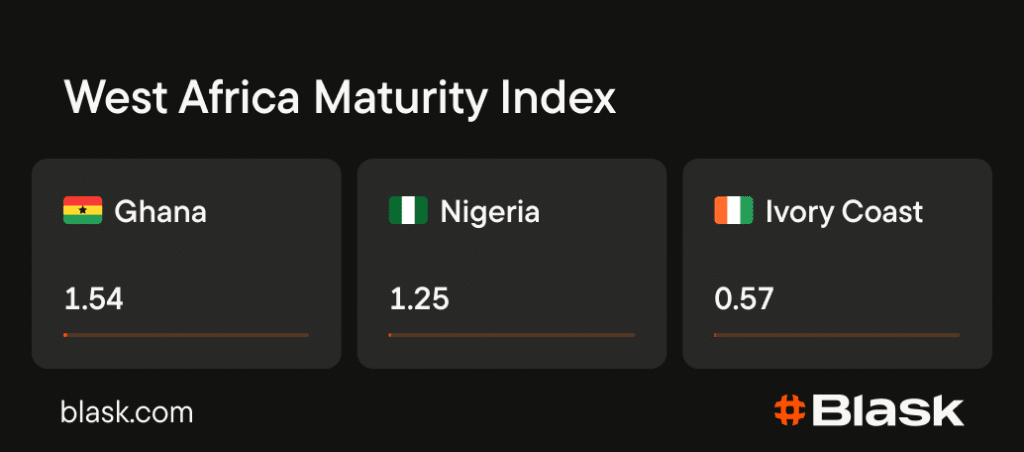

West Africa

West Africa is the most uniform region in this review. Ghana leads, Nigeria follows closely, Ivory Coast trails. Online Betting is the top category across all three.

Nigeria’s position warrants context. It is one of the most actively tracked markets in sub-Saharan Africa by brand count, yet its MI sits below Ghana’s. A market that size, with that many operators competing for attention, still runs primarily on brand recognition rather than category exploration. Ivory Coast has the least developed category demand of the three.

Read Also: Tanzania’s gambling market: one category dominates non-brand search

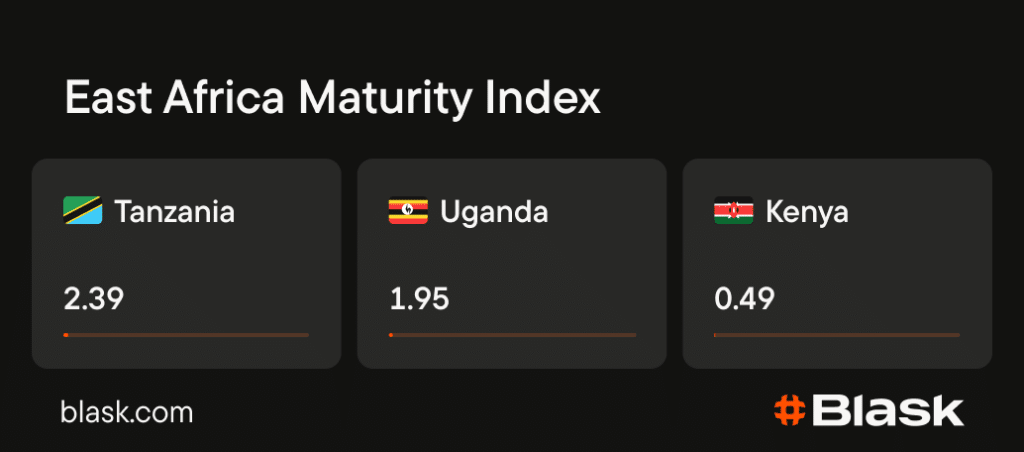

East Africa

East Africa has one of the more counterintuitive results in this data. Kenya, widely cited as the region’s leading iGaming market, has a notably lower MI than Tanzania and Uganda. Online Betting leads in all three.

Tanzania is the regional leader by non-brand demand. Uganda’s MI has grown consistently through the first half of 2025 and now outpaces its neighbours. Kenya’s score reflects a market where brand recognition drives most search behavior, with limited category-level demand by comparison.

Central Africa

Cameroon is the standout in Central Africa and ranks among the top markets on the continent overall. Its MI puts it ahead of any West or Southern African market in this review. DR Congo follows at a distance, and Gabon has one of the lowest scores in the dataset. Online Betting leads all three.

The gap between Cameroon and Gabon is one of the widest within any single region here. Both are small markets by global standards, but their category demand profiles are structurally different.

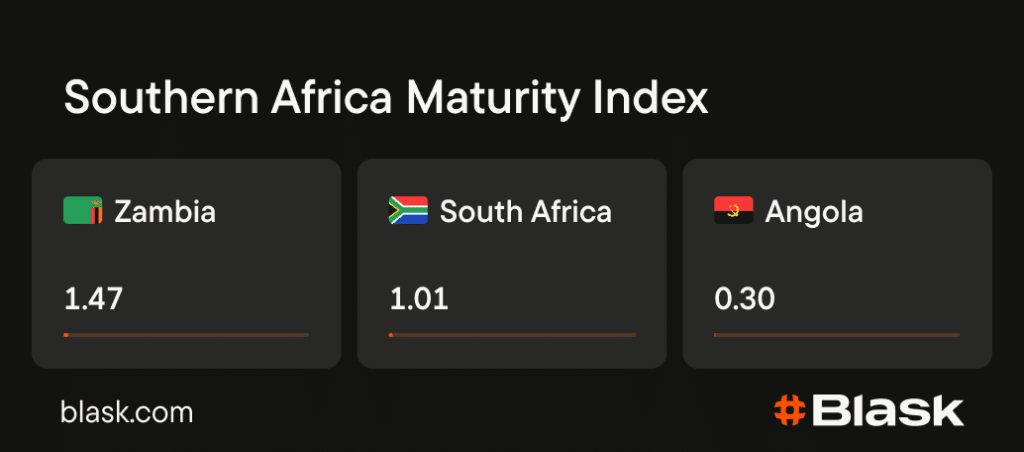

Southern Africa

South Africa has the most developed gambling infrastructure on the continent, yet Zambia leads the region on MI. Online Betting is the top category in all three markets.

Angola has the lowest MI in this entire review. Demand there is almost entirely brand-driven. South Africa reflects a market where brand loyalty still shapes the majority of player behavior, despite its regulatory maturity and operator density.

Bottom line

Africa is a brand-demand continent. Across every region covered here players search for operators, not categories. The Maturity Index stays low almost everywhere.

Arab Africa breaks that pattern most clearly. Egypt’s Fantasy-led demand signals a player base that has developed preferences beyond brand recognition. Cameroon and Uganda show similar movements at a lower level.

For operators, brand-building remains the primary lever across the continent. In markets where category demand is developing, product differentiation starts to matter alongside it.