Three iGaming brands account for more than 90% of BAP, while betPawa captured more than half of users’ demand.

DR Congo is one of the most underleveraged iGaming markets on the continent. A population of 115 million, a licensing path that actually works, and a competitive field of just 36 active brands — compared to the hundreds crowding Nigeria or South Africa.

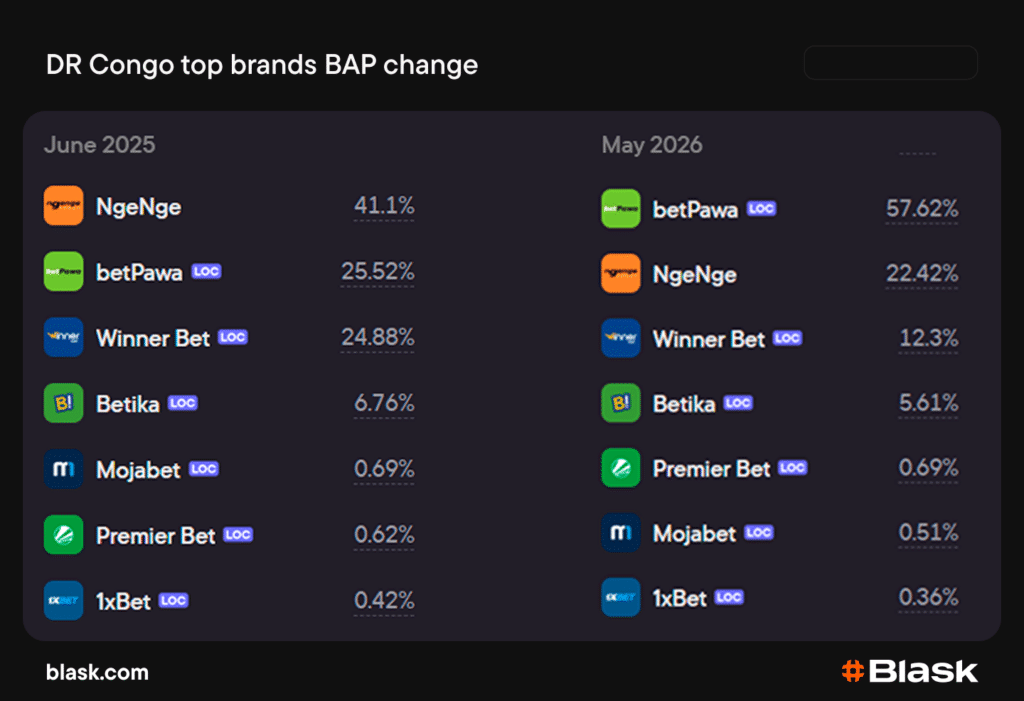

Someone noticed early. Over the past year, betPawa more than doubled its market share, going from 25% to 52.8% of total player demand. That kind of move doesn’t happen by accident.

In this analysis, we look at how DR Congo’s regulatory framework is taking shape, what drives seasonal demand, and who controls the competitive field today.

Macro snapshot

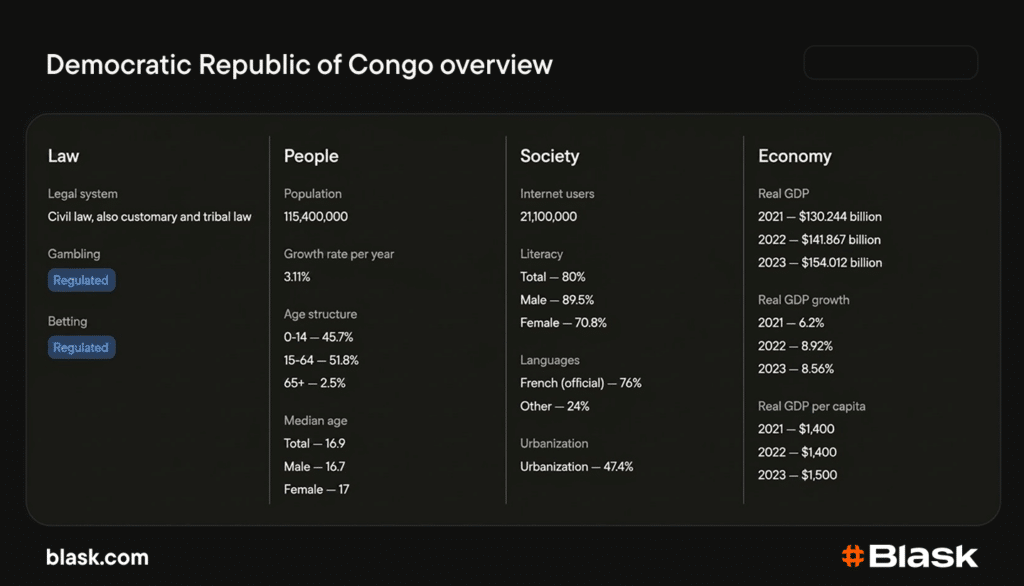

DR Congo’s population stands at 115.4M, with a median age of 16.9, one of the youngest profiles Blask tracks globally. Internet users number 21.1M, representing a penetration rate of roughly 18%. The market has not realized its full potential yet, and the number of players will grow as this country will go savvy.

Regulation: compliance deadline meets a reform in transit

Local market is regulated on paper and chaotic in practice. Sports betting, lotteries, casinos, and prediction games fall under the Ministry of Finance, with SONAL (Société Nationale de Loterie) acting as the mandatory state lottery partner for private operators.

The framework is functional enough to license operators, but enforcement has lagged behind a sector estimated at $1.7B annually, of which the state captures only a $1M (less than 0.05%).

The single most important regulatory dynamic right now is the compliance push. On March 5, 2026, the Finance Ministry ordered all gambling operators to register with the Directorate of Financial Regulation by March 31, 2026 or face fines, suspension, and criminal prosecution. At the same time, authorities are deploying a centralized monitoring platform to track wagers and winnings in real time.

Key timeline:

- March 13, 2018 — ordinance-law establishes central government duties and levies on gambling activities.

- December 14, 2021 — ministerial Order No. CAB/MIN/FINANCES/2021/020 defines practical conditions for granting gambling authorizations.

- April 11, 2025 — Council of Ministers adopts a draft bill establishing foundational principles for games of chance and gambling; transmitted to Parliament in June 2025.

- February 11, 2026 — National Assembly member Willy Mishiki Buhini tables a separate parliamentary bill targeting online gambling regulation.

- March 2026 — Finance Ministry compliance deadline; monitoring platform deployment begins.

Tax stack for operators

Sports betting operators face an estimated 20% GGR tax, a 10% withholding tax on player winnings, and an annual operating license tax capped at $100,000 under a November 2019 ministerial order. Private operators must also partner with SONAL, which reportedly takes a revenue share on gross gaming revenue. A pending reform bill proposes mandatory player accounts and real-time tax reporting to close the collection gap.

Licensing paths

Two paths exist in practice. Operators obtain ministerial authorization through the Ministry of Finance under Order No. CAB/MIN/FINANCES/2021/020, and private entities must secure a partnership with SONAL before going live.

There is no standalone online license. Blask tracks 36 active brands in the market; the majority of the top ten are locally embedded operators, not offshore license-holders.

Regional position: Central Africa’s second-largest market by CEB

DR Congo ranks #9 in Africa by CEB at $140.82M, being close to Senegal ($143.26). DR Congo trails Cameroon ($182.33M) as the second-largest market in Central Africa.

The implication is scale without saturation. DR Congo’s 115M population and 32.7M APS give it a large addressable base, but with only 36 active brands versus the hundreds competing in some African open markets.

Market dynamics: trough opening, AFCON lift, betPawa surge

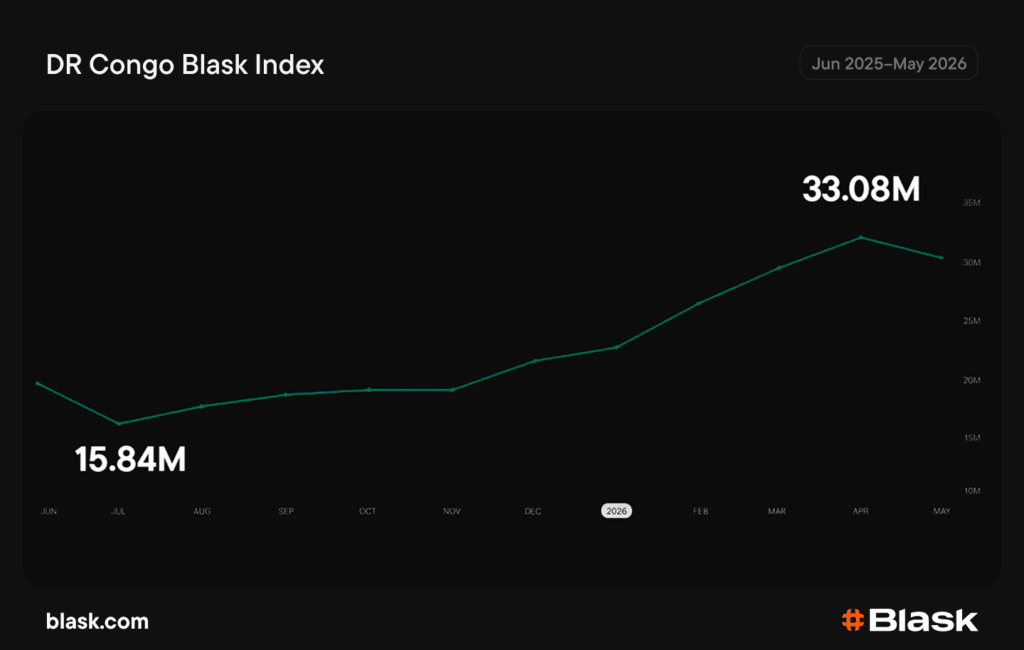

DR Congo’s Blask Index for Jun 2025–May 2026 opens in the European off-season and closes at the period’s highest competitive intensity. Three phases define the year.

Opening trough (Jun–Jul 2025). July is the weakest month in the entire twelve-month window. European leagues were in off-season after the 2024/25 Premier League concluded on May 25, 2025, leaving no major club football anchor through the Congolese summer.

Football-driven recovery (Aug 2025–Jan 2026). The 2025/26 Premier League kicked off on August 15, 2025, reversing the decline within weeks.

AFCON 2025 in Morocco, running from December 21 to January 18, added a continental layer: DR Congo opened Group D against Benin on December 23 and reached the Round of 16 before losing to Algeria on January 10.

Consolidation surge (Feb–Apr 2026). Demand accelerated sharply as betPawa captured a share. April became the period peak; May softened to 30.25M, but the competitive reordering was complete: betPawa held 52.8% BAP against NgeNge’s 23.2%.

Blask Index rose 109% from the July trough to the April peak, with the steepest climb concentrated in the final quarter of the data period.

Competitive landscape: betPawa breaks away in a three-brand market

DR Congo’s competitive structure collapsed toward a single leader across the data period. betPawa, NgeNge, and Winner Bet held a combined 93.11% BAP by May 2026. The market is turning into a concentrated oligopoly moving toward a near-monopoly.

A dramatic market shift unfolded as betPawa surged from 25.52% to a dominant 57.73% BAP by May 2026, securing a commanding $6.65M in CEB. This rise came at the direct expense of former leader NgeNge, whose share plummeted from 41.1% to 22.42%, leaving it trailing in revenue at $3.5M. Meanwhile, Winner Bet also lost ground, shrinking from 24.88% to 12.3%.

The long tail is negligible. Brands outside the top ten account for less than 0.5% of combined BAP. For new entrants, the barrier is not regulatory access alone. The Ministry of Finance licensing path is achievable.

The barrier is competitive: breaking into a market where the leader already commands more than half of total player attention, and the top three control nearly nine-tenths of it.

Read Also: Ethiopia’s casino market runs on crash games

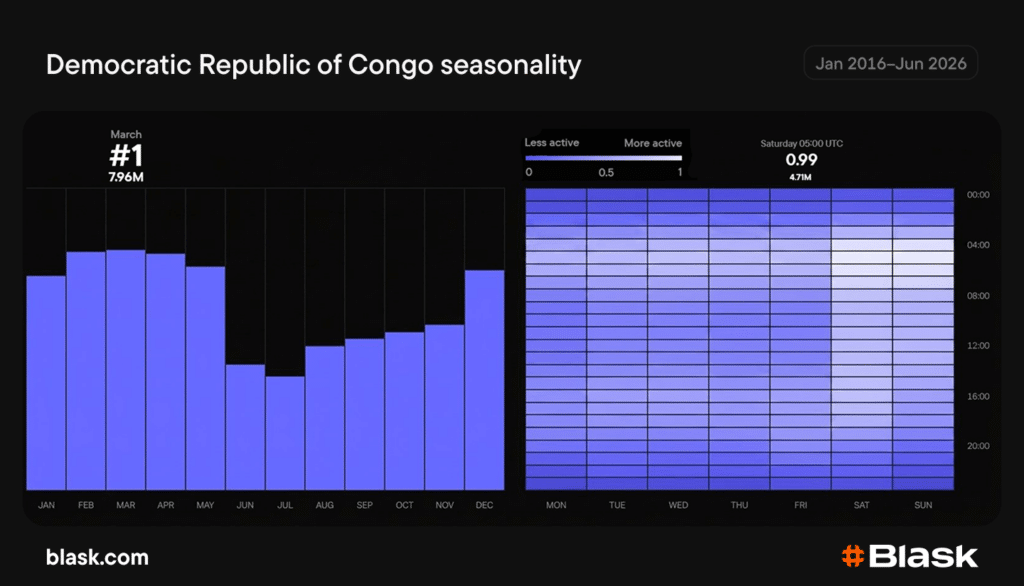

Seasonality: football calendar with a spring peak

The weakest window runs from June through August, bottoming in July when European leagues are in off-season. Demand recovers from September onward with the peak in March. April and May rank second and third.

Saturday and Sunday dominate the weekly heatmap, with Saturday registering the highest total activity across the period. The peak hourly band sits at 05:00 UTC, consistent with morning betting ahead of the European weekend fixture slate reaching Congolese audiences. Monday is the quietest day of the week.

Conclusion

The Finance Ministry’s compliance deadline, the monitoring platform rollout, and two legislative tracks in Parliament will reshape the rules for every operator currently active.

The competitive order is not frozen. betPawa’s rise from 25.52% to 57.62% BAP proves that dramatic share shifts happen even in concentrated markets. NgeNge’s retreat from 41.1% to 22.42% shows incumbents can lose ground quickly. However, movement remains available to operators who localize effectively and move before the framework hardens.

DR Congo rewards operators already embedded when regulation catches up. The market is young, mobile-first, and football-driven, and the operator holding majority demand today is best positioned to define what comes after the reset.

About Blask

Blask is an AI-powered platform for iGaming and gambling market analytics. The company turns fragmented open-source signals into real-time insight on brand visibility, player demand, and baseline revenue metrics, helping teams move first, spend smarter, and reduce risk across global markets.